Step 1 - Understanding the Fundamentals

It is a pretty simple question, which most people would answer with "to make money" - and they wouldn’t be wrong; however, I think the more valuable question to ask yourself is why have you chosen property investing compared to other asset classes such as shares.

Now that is not to say the two are mutually exclusive - I personally invest in both property and shares; however, given how capital intensive property investing is compared to stock investing for the average person (with an average income) it often naturally results in you putting your eggs more in the property basket.

I am not going to get into the great Australian debate of property vs shares because:

(1) I am not a financial advisor (and this is not financial advice); and

(2) the answer can be different for each person.

However, for those you who are interested in that debate - you can check out the below series from the Suburb Data podcast. What I am going to do though is highlight a few key differences so that you know what you are getting yourself into when you start property investing and why it can be a powerful investment class for the average person.

Power of Leverage

However, the administrative inconveniences involved in property investing are far outweighed by the returns you can achieve through the use of leverage. Leverage is when you borrow money to control an asset that is worth more than your cash investment. Or in other words, if you take a mortgage out with the bank to buy a house worth $500,000, of which you only needed to provide $100,000 yourself (i.e. a 20% deposit) - that is you taking advantage of leverage.

The primary advantage of using leverage is that it can significantly increase your returns, because instead of you making a 5% return on your cash deposit of $100,000 - which would be $5,000, you would instead be making 5% on the $500,000 asset you purchased - which would be $25,000, and compared to the amount of cash you actually invested that is in fact an impressive 25% return (i.e. a $25,000 gain on a $100,000 deposit = a 25% return) - this is known as your 'cash-on-cash return'. Calm down finance bros, yes I know this doesn't take into account holding costs - I am just trying to explain a concept here!

I know I said I wouldn't compare property vs shares but bear with me. We know that the long-term average return on Australian shares is 9.8%, whereas for Australian property it is 6.3% (this increases to about 8.3% when you add on rental income and adjust for ongoing costs like maintenance etc.). So at first glance it looks like shares are the clear winner; but not so fast, let's take a look at the power of leverage over a longer time horizon.

Active vs Passive Investing

The first thing you need to know about property investing is that it is more of an active investment strategy. I know the gurus like to use the words 'passive income' and property investing in the same sentence - but that is a bit misleading in my opinion. Here is how I like to look at it: in property investing you are not just buying an asset (i.e. the land), you are also buying a mini-business (i.e. the house) that needs regular attention. Whilst there are steps you can take to make property investing as passive as possible, there are always things you will be ultimately responsible for to ensure that your mini-business is operational - such as choosing tenants, responding to maintenance requests, mortgage repayments, council / rates payments and so on. Yes, a property manager can help you with a lot of this, but ultimately they will still rely on you to make the final call - you are the CEO of this mini-business and the buck stops with you.

In all honesty, if you choose the right investment and build the right team around you (which I will try help you with throughout this website), property investing in reality is not that much work - it is not a daily / weekly thing you need to manage. There are periods where there can be more headaches than usual, typically during / shortly after making a purchase, and then there are times where it all falls into place nicely and you don't have any issues for months. I am saying all of this is just so you understand that property investing is not a truly passive investment strategy like the stock market - where you can buy some shares from a brokerage app on your phone and that’s it, there is nothing else required of you (believe it or not but the CEO of an ASX 200 listed company does not give you an invite to the board just because you bought a few shares).

As you can see from the above table, even though shares have a greater average return than property, as a result of leverage you end up with an additional $1.4 million through property investing over a 30 year period (and this is just with one property, imagine if you can build a portfolio of 2 - 4 or even more).

Before I get blasted by some dorks on reddit, please note that this example has excluded rental income for the property returns (i.e. the 6.3% average return was used, not 8.3%) and yes I am aware that these numbers don't include holding costs such as mortgage repayments - whilst not insignificant you can see from the gap between property and shares that there is still a lot of leeway to include these and the leveraged asset (i.e. property) will still come out ahead.

For reference, you can actually use leverage to buy more shares; however, in reality most banks will not allow the average person access to borrowed funds to purchase shares as they are inherently more volatile and are therefore considered higher risk (not financial advice…). The leverage limits on shares is also around 50% - 70%, whereas for property you can comfortably borrow anywhere from 80% - 90% of the value of the property (sometimes more) due to its generally lower price volatility (again… not financial advice).

Good Debt vs Bad Debt

Despite clear evidence on the returns you can achieve with using leverage, some people are quite uncomfortable with holding a lot of debt - which will be impossible to avoid if you are trying to build a sizeable property portfolio.

I don't blame people for feeling this way, it can be daunting for some - but I believe this anxiety generally comes from not understanding the difference between good debt and bad debt.

Note: this may be news to some of you, but the loan on your family home (i.e. PPOR) is generally not considered good debt by the banks - whilst it may go up in value, it does not produce you an income and the interest on your mortgage is not tax deductible.

Impact of Inflation

I haven't included it in the table above as I think it requires a bit more explanation to fully grasp, but another benefit of good debt is that whilst the value of the asset increases the value of the debt also decreases. No, I am not talking about you making repayments to the bank, I am referring to the impact of inflation on the real value of debt.

Whilst we have all heard of this infamous 'inflation' before, for those of you who aren't sure of its meaning, it is essentially the general increase in the price of goods and services over time which then decreases the purchasing power of money. Or in other words, $1 today will buy you less and less over time. This is something that probably hits hard to most Australian's today, whether they know it or not. If you take a walk through your local Coles or Woolies you will notice that what you can purchase with a $10 note today is no longer enough to feed a family of four (sorry Curtis Stone!) - it's barely enough for one person, which means whilst $10 is still technically $10 it is worth less because you cannot buy as much with it.

Inflation does the same thing to debt. If we scroll back up to our example table with the $500,000 house, this means that the real value of that $400,000 you borrowed from the bank is technically decreasing in value over time because whilst it looks like the same amount of money on paper, what you can buy with $400,000 today will be significantly less than what it can buy you in 30 years' time - so in other words, the value of the debt has decreased due to inflation (please remember this concept, it will be relevant again when we discuss whether you should opt for an interest only loan or a principal + interest loan).

Also, don't forget what happened to the value of our $500,000 house in this time - it increased to over $3 million.

That is the power of leverage and good debt.

For the smart students in the class, you may have picked up that inflation must also do the same thing to the cash we have saved in the bank - if so, you would be correct. Inflation also devalues your cash savings, which is why it is vital that you deploy your cash (to the extent you can afford it) into appreciating assets (such as property... and shares).

I won't labor on this specific point much as given you are reading a website on property investing I assume you know the importance of investing to beat inflation, but for anyone interested please take a look at this video from PK Gupta which I believe gives an interesting summary of the impact of inflation / currency debasement on real wages and asset values (I know the title is giving doomsday vibes but it's a good watch).

Negatives of Leverage

It would be irresponsible of me to rave on about the advantages of taking on debt without also mentioning the negatives (albeit I am not a financial advisor and this is not financial advice!). Whilst we may characterize something as 'good' debt, it's important to remember that it is still debt at the end of the day and it is important to ensure that you do not overleverage yourself to a point where your mortgage repayments put you and your family into more financial stress than you can handle - I am not just talking about the impact on your credit file, I mean your general wellbeing.

As we have seen recently, things can change very quickly in the world-economy and it is vital that if you are going to take advantage of leverage that you also take the proper precautions to ensure something like interest rate rises do not result in you going into financial stress. One thing that I always ensure that I have which helps me sleep at night, irrespective of my large debt balance, is having an emergency fund of 6 - 12 months of living expenses (including my mortgage repayments and unexpected costs such as tenant vacancies).

Lastly, the whole rationale of 'good' debt and using leverage is that you use it to purchase an 'appreciating asset'; however, that is not guaranteed in the property market (or the stock market) - plenty of Australian's take out mortgages each day and use the money to buy horrible investment properties. Why? Because they aren't educated and as I have said before, everyone thinks they are a property expert despite not investing any time in the most important piece of real estate they own: the 6 inches between their ears.

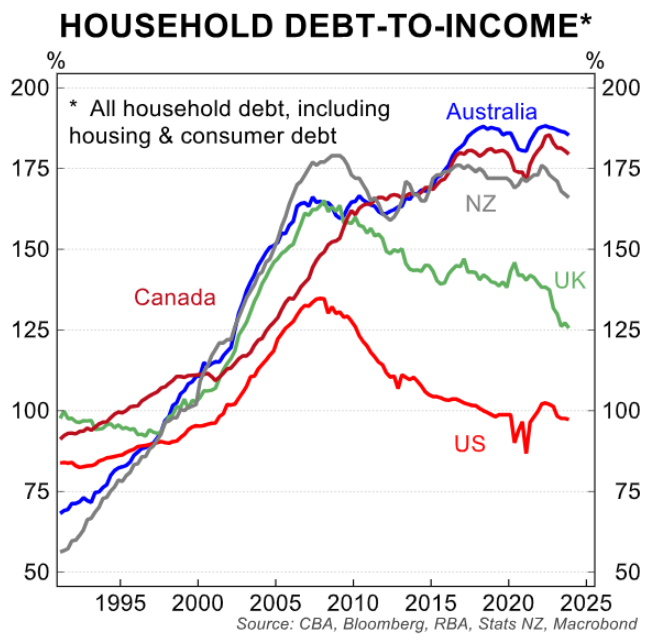

This is extremely concerning given Australia has some of the heaviest leveraged households in the world (see the below graphs for context). So in my opinion, one of the smartest things you can do to minimise the negatives of leverage and maximise its benefits is educate yourself on property investing before asking the bank for money to buy one.