Step 5 - Property Sourcing and Selection

Now that you know how to source properties, it is important that we go through the criteria that you want to ensure your property has and those red-flags that you need to avoid.

Similar to the Step 4 suburb selection method you will see that each of the below criteria also contains a flexibility metric so you can confidently make trade-offs where possible - which you will need to do because no property is perfect, there will always be some issues.

Again, I am feeling very generous and have linked a spreadsheet that you can use when assessing properties against this criteria.

For reference, this isn't absolutely everything you can look for, these are just the most important and things that many people don't check. You will notice I haven't included things like proximity to shops, schools, public transport etc. because these factors are not that important. You can still look at them (generally want those amenities to be within a 1km - 5km radius) but they are highly flexible and you shouldn't be making investment decisions based solely of those lifestyle factors.

Criteria

Housing commission / social housing

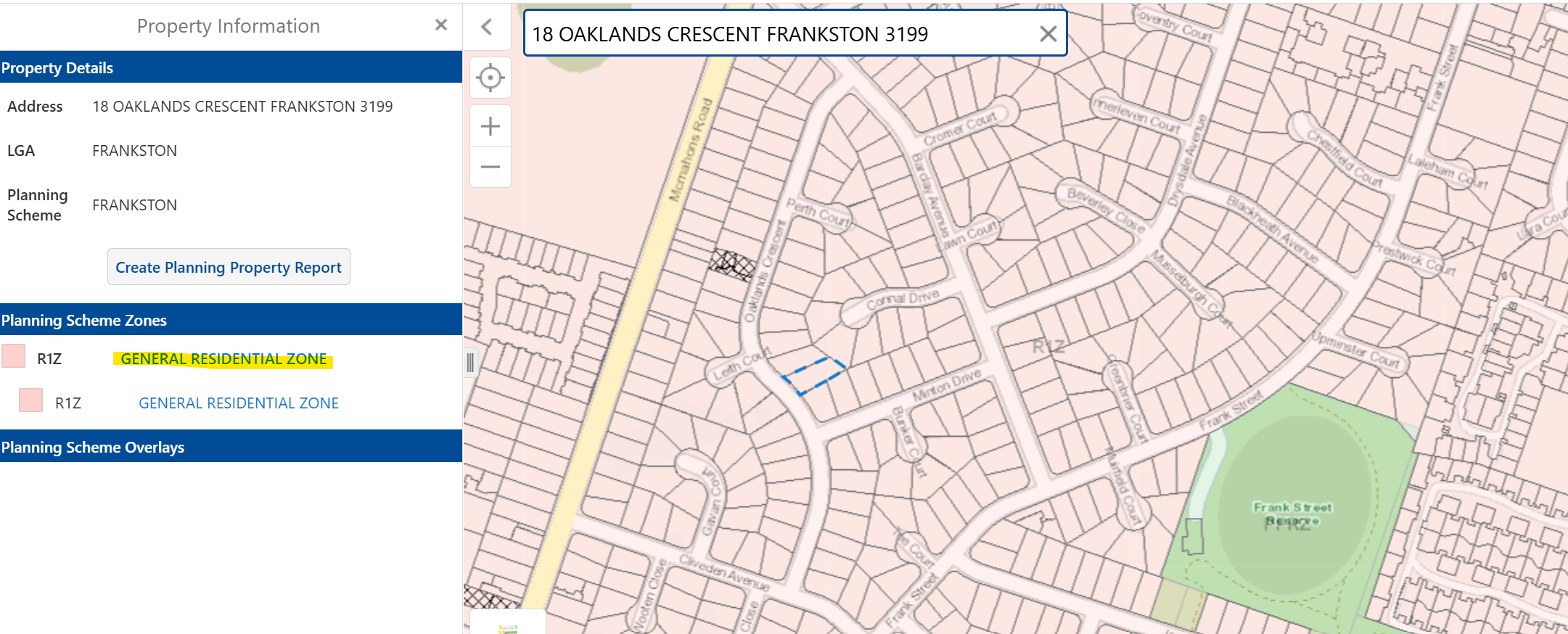

Council zoning

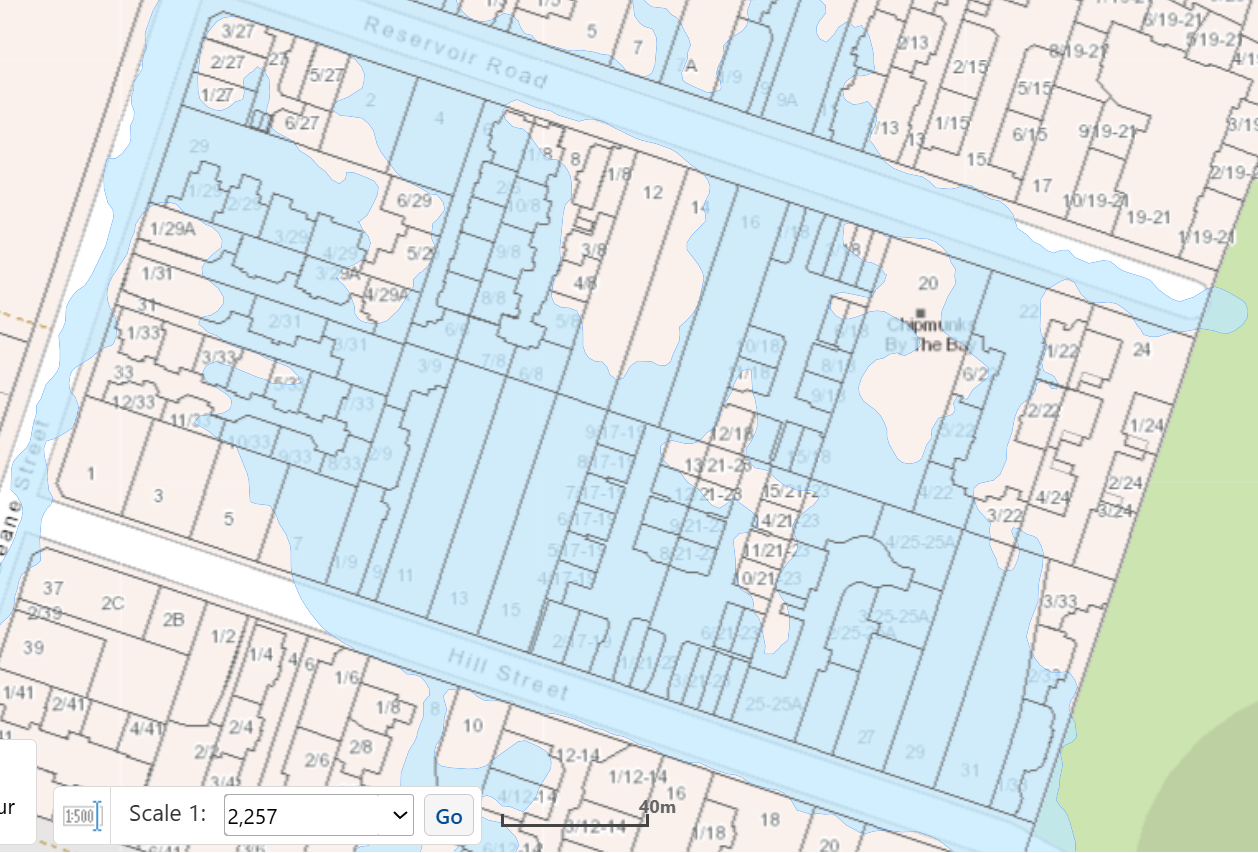

Flood zones

Bushfire zones

Heritage overlays

Flight noise corridors

Land-to-asset ratio

Main / busy roads

Commercial / industrial properties

Bedroom size

Easements

Source

Free: Microburbs, OpenStats, local property managers

Free: go to the relevant council website, they will have a planning map. You can also call the relevant council.

Free: go to the relevant council website, they will have a planning map. You can also call the relevant council.

Free: Council planning websites

Free: go to the relevant council or airport noise tool for the state.

You can also check with local property managers.

Free: Most state governments have websites to identify land value. E.g. QLD

You can also look at recently sold 'vacant land' on realestate.com.au - use this if the valuation on the state government website is very old.

Free: Google street view.

You can also check council planning website and call local property managers if you aren’t certain if it is a busy road.

Target Range

Low - beneath 10%

We want to be at least three streets away from high % pockets of social housing.

Example: see the below screenshot from Microburbs, that area in red has a social housing concentration of 15% (this percentage will show when you hover over the area on the website), meaning we want to avoid it. However, the areas in green around it we are comfortable with as they are around 0-5% which is totally fine.

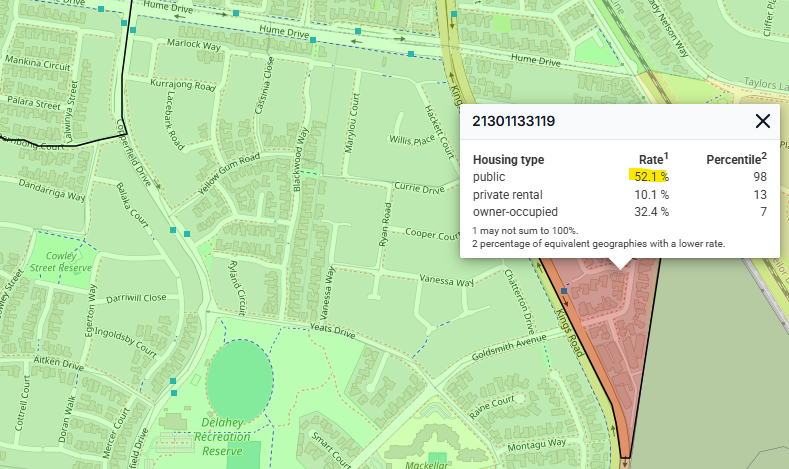

Example: here is an another example using OpenStats, I quite like this website as you can also easily see the data on which pockets have high concentrations of owner-occupiers.

In the below example you can see that the pocket in red has 52% social housing, which is extremely high - this means we want to make sure we are not buying in this pocket and if we are buying in a green zone close to it then we should double-check with a local property manager to ensure we won't have any issues.

Example: please see below screenshot which shows an area that is largely "general residential zoning" (i.e. shaded pink).

Property not in a bushfire zone.

Example: please see below screenshot which shows those areas in orange as the properties impacted by bush fires.

None, unless they have minimal restrictions on what you can do to your property or if they are normal for the area.

Flexibility

Low

Noting that if your property has no blue shading and your neighbor does, then that is generally fine - we just want to avoid the properties which have blue shading on them.

If there is only a tiny bit of a property which is impacted by flooding and it doesn't impact the actual house, then you could potentially compromise on this if the area has never experienced a flood, but you should check insurance quotes to make sure they are normal.

Flood zones may reduce the property's potential for capital growth. The obvious risk is also that it may flood one day and be very expensive to fix and the insurance premiums can be high.

Bush fire zones may reduce the property's potential for capital growth. The obvious risk is also that there may be a bush fire one day and be very expensive to fix your home if there is any damage and the insurance premiums can be high.

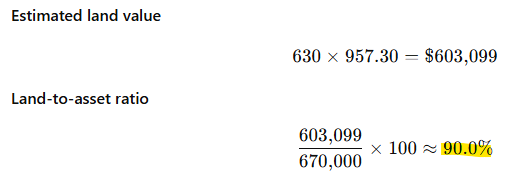

As you can see, the land-to-asset ratio of the above house in Hoppers Crossing is around 90% which is well above our threshold. But as I said above, you didn't really need to go through this entire calculation because you can tell the house is more than 15-20 years old and its land size is above 450m2.

Low

A few housing commission homes is totally fine (and actually quite normal), but you need to avoid the high density areas.

Low

Noting that if your property has no orange shading and your neighbor does, then that is fine - we just want to avoid the properties which have orange shading on them.

If there is only a tiny bit of a property which is impacted by bush fires and it doesn't impact the actual house, then you could potentially compromise on this if the area has never experienced a bush fire, but you should check insurance quotes to make sure they are normal.

Medium

Rationale

Buying a property in an area with a high concentration of public housing may be associated with less favourable demographic trends and a higher likelihood of crime.

This doesn’t necessarily impact capital growth in the long-term, but it can make getting the property tenanted more difficult.

Low / general residential zoning.

Medium

Provided the zoning doesn’t allow for things like multiple story unit blocks etc. it can be acceptable to buy in areas which allow for medium density like townhouses etc. Depending on your strategy it may even be advantageous as it could increase the development potential of the property.

Medium or high-density zoning near your property can lead to increased traffic and reduced owner occupier appeal.

Free: go to the relevant council website, they will have a planning map. You can also call the relevant council.

Property not in a flood zone.

Example: please see below screenshot which shows those areas in light blue as the properties impacted by flooding.

None to very minimal, noting the focus is on the noise impact not if it is just in a flight path corridor.

The old test that some people use is that if it is loud enough to interrupt a conversation at a family BBQ then that will be an issue, some minor airport noise is generally ok.

Greater than 50% - in other words, we want the land the house sits on to be worth more than 50% of the proposed purchase price.

As a general rule, houses which are 15-20 years or older and sitting on more than 450m2 will generally always meet this threshold. This can be useful to know if you don't want to calculate the land-to-asset ratio for every property you look at.

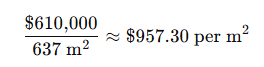

Using the realestate.com.au method as an example (but just looking up the value of land on government websites is easier…), we can see that the below 637m2 block in Hoppers Crossing sold for $610,000 in Aug 2025, so this is a very recent example of land values in the area.

https://www.realestate.com.au/sold/property-residential+land-vic-hoppers+crossing-204224032

If we divide the sold price by total size of the block, this will give us the "price per square metre" in the area, which is $957.30.

Try look at a few other blocks in the area of your home which have sold recently to see if they compare. Remember not all blocks were created equally - don’t compare blocks next to a train line or close to the water as they are valued differently.

Then let's take a look at an example listing in the area, see the below house which is a few streets away and is 630m2 and sold for $670,000.

So a vacant lot of 637m2 sold for $610,000 and a house nearby on 630m2 sold for $670,000 - it is immediately obvious here that the land-to-asset ratio is well above 60% as you are almost getting the house for free. But let's do the calculation anyway.

All you need to do is multiply the price per square metre by the land size of the house, then divide that figure by the asking price / what you are willing to pay then times it by 100 to get a percentage. See the below for example (again using ChatGPT).

A property located on a main road or major thoroughfare is more likely to experience higher noise levels and traffic congestion, which can negatively impact capital growth.

T-Junction / Roundabouts

Cemetery

Train tracks / stations

Proximity to high-voltage power lines and substations

Free: Google street view.

Free: Google maps

Free: Google maps

Free: Google maps

Free: Google street view

Avoid all main roads and busy thorough fare roads.

This includes being located on the same road as a school, bus route, shopping precinct or gathering place (i.e. sports field, church, childcare) - as this will significantly increase the traffic on the road during certain times.

Example of a main road

Example of a thorough fare road

Avoid buying properties at the end of a T-Junction or directly on a roundabout.

Example of a property at a T-Junction:

Example of a property on a roundabout

1-2 streets away from any commercial / industrial properties (e.g. warehouses, waste management plants, logistic companies etc.)

1-2 streets away from any cemeteries.

At least 200m -300m away from any train tracks and associated noise.

Ideally, these are not even visible but we want to at least be 300m - 400m away.

Example of high-voltage power lines:

Medium

In areas where heritage controls are common and have minimal impact, they may be an acceptable consideration.

Low

If you are buying units / townhouses it may be difficult to meet this threshold, in which case you need to try maximise the land-to-asset ratio as much as possible by only buying into unit blocks / complexes with a handful of dwellings - this will also mean your strata costs will be minimised as a result.

Low

Low-Medium

If the T-Junction is at the end of very quiet street, like a cul-de-sac, or the roundabout isn’t a busy one then that can be ok.

Low

Low

Low

Low

Heritage overlays can restrict renovations and development, limiting a property’s future potential.

Properties located within flight path noise zones may be less appealing to both tenants and owner-occupiers.

As we discussed in Step 1, land appreciates and buildings depreciate. Which means it is critical that the majority of the property value is in the land component.

An intersection can create extra noise and headlight glare through windows.

There is also more risk of cars crashing into the property.

Commercial and industrial areas typically generate higher levels of traffic, resulting in increased noise from deliveries, customers, late-night operations, and heavy machinery - which is generally not attractive to future buyers and tenants.

Purchasing a property next to a cemetery is generally not attractive to future buyers and tenants

Living near train tracks is not attractive to future buyers and tenants because of ongoing noise and vibrations.This makes these properties quite difficult to sell which is why they are much cheaper to purchase too.

These will hurt your re-sale value and ability to find a tenant as they are unsightly.

Power poles, street light poles, bus stops

Free: Google street view

Not directly in front of the house.

Example of power pole in front of a house:

Medium

If it is a good deal, this is something that you could compromise on a power pole / street light, especially in very hot markets.

However, if it is a bus stop, then you shouldn’t be compromising on this at all in my opinion.

This impacts the re-sale of the home as it makes the property less visually attractive, especially compared to other houses in the street.

Bed-bath-car configuration

Paid: HtAG

Free: Realestate.com or Domain

Choose configurations which are the most popular or have a lot of demand, the most important thing is the amount of bedrooms. The most common configurations are: 3 bed / 1 bath, 3 bed / 2 bath, 4 bed / 2 bath.

Bedrooms: if 4 bed houses are the most popular in the area, your preference should be to get a 4 bedroom home. HtAG gives you this data, but if you want a free option look at realestate.com.au or Domain and see whether 3 bed or 4 bed houses have sold more this year, this will tell you which is most popular. E.g. for the suburb of Strathpine. Noting, you can still go with the second most popular bedroom configuration if demand is strong.

Bathrooms: a 3-bed and 1 bath is generally fine but normally a 4-bed and 1 bath usually lacks functionality. Check with local property managers to confirm if there would be any issues with renting a home with only 1 bathroom.

Car spaces: you generally need at least a carport for 1 car, lock-up garages are more preferable but it typically isn't a deal breaker. Check with local property managers to confirm.

Low

Flexibility is low in the sense that I wouldn’t be buying anything below a 3 bedroom house.

Noting you may be fine with a 2 bed unit or townhouse if they are very in demand.

If a property does not align with the preferences of most renters and buyers, it is more likely to experience longer vacancy periods and attract fewer future buyers, ultimately limiting capital growth.

Free: floorplan on relevant listing

At least 3m x 2.7m

Low-Medium

If it is just one room which is slightly smaller than this then it can be something you compromise on

Small rooms can be a drawback for both renters and future buyers.

You need to be very careful as some homes marketed as four bedroom properties are actually three bedrooms with a small study.

Smaller bedrooms are also taken in consideration by valuers when they value the property.

Shape of land

Free: Google maps or property listing

Square or rectangle shaped block and no irregular shaped blocks.

Example of irregular shaped block:

Medium

You can flexible on this if it is in a court, cul-de-sac or just generally a good deal.

An unusually shaped block can limit development potential and reduce the land’s functionality, which may negatively impact its overall value.

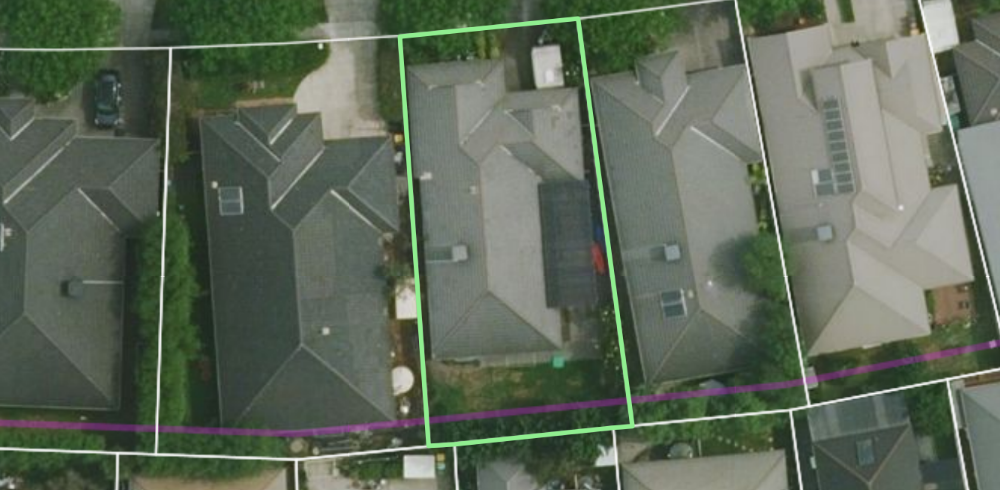

Subdivided / battle-axe block

Free: Google maps

Avoid any houses which have been subdivided and / or have a separately sold house on the same block of land.

This is usually identified by having a letter in the name of the property (e.g. 24A, 24B).

Example of subdivided / battle-axe block:

Low

The block at the back (battleaxe block) lacks street appeal and can make selling the property more challenging and limit its capital growth.

The front block will also have cars entering and leaving at all hours and often lacks privacy.

Slope of land

Free: Archistar, Council website planning tool

None (i.e. we want a flat block) or less than 3m

Medium

A steeply sloped site raises development costs, increases maintenance expenses and is not attrative to tenants or buyers who are seeking a flat yard for children.

Dwelling orientation

Free: listing advertisement, Google maps

North facing

High

This is a nice to have and is not a major deal, it can be a bit more important sometimes for units and townhouses.

Properties with main living areas oriented to the north receive the most sunlight compared to other homes.

Owner occupiers are very drawn to this and it may demand a premium when you go to sell the property one day.

Dwelling floor plan

Free: listing floor plan

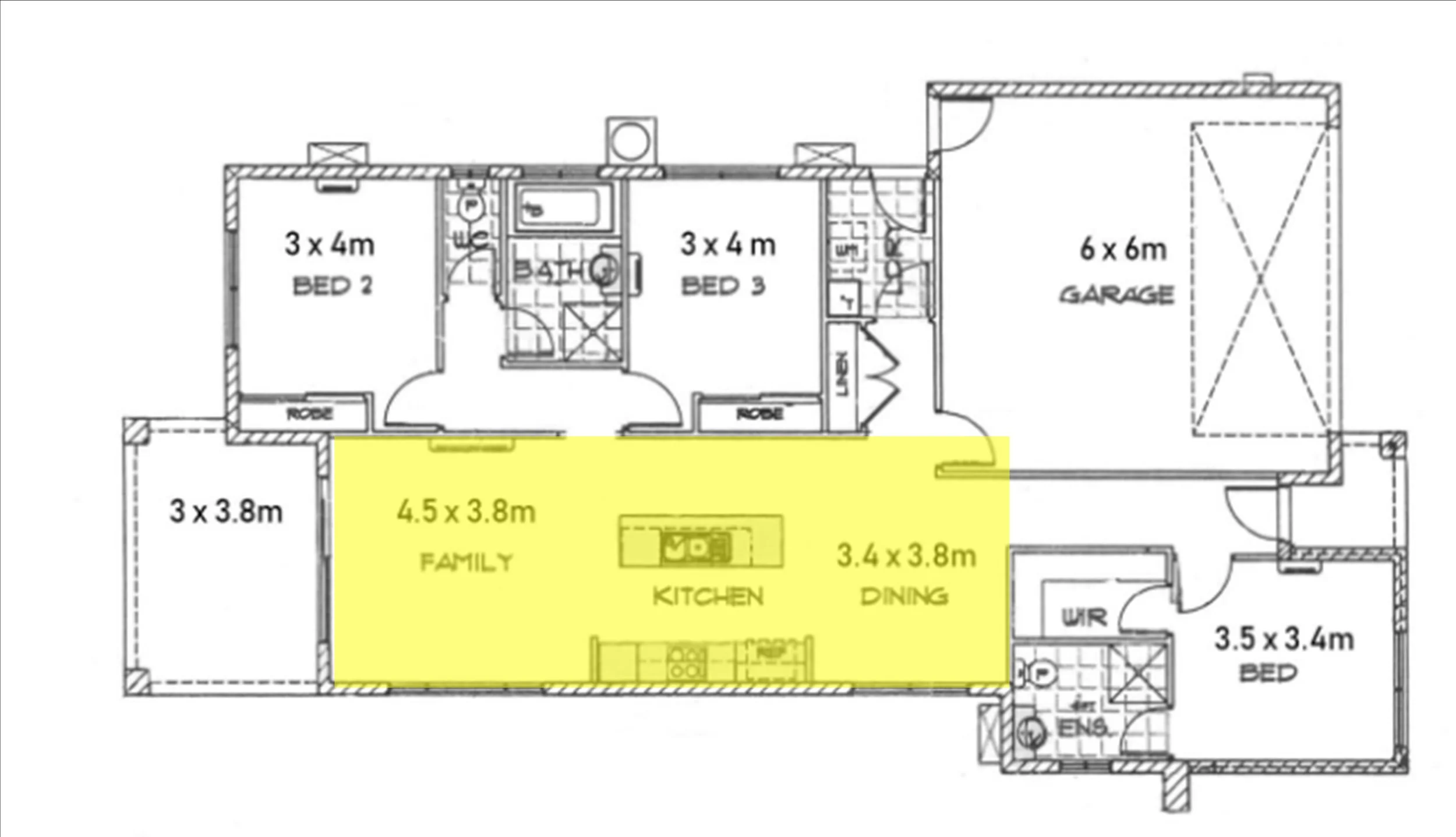

Open plan - i.e. kitchen and dining / living area connected and not in separate rooms.

Examples of open plan living floorplans:

High

You will find old houses will rarely have open plan living floor plans, it is not a major deal so this is flexible.

Most people prefer kitchens that are open to the living or dining areas and therefore these types of properties can achieve a premium when you go to sell.

Free: Archistar, Council planning websites, Title search (noting that your conveyancer should be assisting you with this search).

No restrictive easements running through the middle of the block or in areas that restrict building potential.

Side or rear easements are typically fine if they don’t affect usable space in the back yard - especially if you don't plan to develop the land.

Example of rear easement:

See the below purple line, this is a sewer easement which is generally quite common and not considered an issue.

Medium

Be sure to talk to your conveyancer on the actual impact that any easements may have on your property and whether it is typical for properties in your area.

An easement that restricts the ability to develop may limit capital growth in the future and will reduce your options if you wanted to develop the land as an exit strategy.

Insurance quote

Pool

Free: AAMI, Allianz, other applicable building insurance providers etc.

Free: Google maps, listing advertisement

Average or below the average price of the insurance quote for the area.

You can assess the average insurance quote for the area through general google / ChatGPT research or by conducting insurance searches on other properties in the area near your relevant property.

Example of AAMI insurance quote:

No pool, unless it is highly desirable for the area in which case it can be acceptable to have a pool (this can be confirmed by local property managers)

Medium

Medium

It’s important that a property’s insurance premium is at or below the suburb average. Higher-than-average quotes may signal underlying risks such as flood or bushfire exposure, and elevated insurance costs can also negatively impact cash flow.

A pool increases ongoing maintenance costs and in most cases, pools do not contribute to capital growth.

Specific criteria for units and townhouses/villas

All of the above criteria with respect to property selection (and the suburb selection data criteria from Step 4) apply to purchasing units and townhouses/villas.

However, there are a few specific things to consider when purchasing units and townhouses/villas in particular:

Land-to-asset ratio: it is unlikely you will be able to find a unit or townhouse/villa which has a land-to-asset ratio of 50%; however, you should be looking for units or townhouses with a land component. For example, for townhouses/villas, if it is 100m2 - 200m2 or more this would be considered to be a solid land component for a townhouse/villa. You may also find this in larger units in blocks of 3 - 6, but otherwise you want to ensure you are buying units in a boutique block/complex.

Boutique block/complex: you want to ensure that you aren’t buying units in high-rise blocks with heaps of apartments, stick with boutique blocks that are 3 stories or less with less than 12 units. The same can be said for townhouses/villas, you want to be staying away from townhouse/villas complexes that have more than 12 townhouses/villas in them - the fewer the better.

Low Strata Fees: you want to be avoiding block/complexes which have a range of fancy amenities such as pools, elevators, theatre rooms, common areas etc. as they will significantly increase the amount you need to pay in strata fees which will impact your cashflow. On the topic of strata, make you get a copy of the recent strata reports to ensure there is no red-flags like large special levies being discussed or major structural issues / maintenance concerns.