Step 1 - Understanding the Fundamentals

Before we get into this section, let me define the key terms for you - because if you don’t understand these the rest of this won’t make much sense.

What is “Capital Growth”

Capital growth refers to the increase in the value of a property over time. It’s the gain an investor makes from the property's appreciation in market value.

How do you calculate it:

Capital Growth ($ figure) = Current Value minus the Original Purchase Price

Capital Growth (total % figure) = Capital Growth ($ figure) divided by the Original Purchase Price, then multiplied by 100

Capital Growth (yearly % figure) = Capital Growth (total % figure) divided by the number of years of growth

Example:

You purchase a house in Brisbane for $600,000.

10 years later, it's worth $850,000.

The capital growth as a dollar value is $250,000.

The capital growth as a total percentage is 41.67%

The capital growth as an annualised percentage is 4.17% per year

If you want to get more technical, please Google / ChatGPT how to calculate your "compound annual growth rate" (CAGR).

What is “Yield”

Yield is how much income the property generates relative to its purchase price, usually expressed as a percentage and either as "Net" figure (i.e. including expenses) or a "Gross" figure (i.e. not including expenses).

How do you calculate it:

Gross Yield = the Annual Rental Income divided by the Purchase Price, then multiplied by 100.

Example:

Rent: $30,000/year

Purchase Price: $600,000

Gross Yield = (30,000 / 600,000) × 100 = 5%

In a residential property investing context, when people refer to "yield" they are often referring to gross yield.

Net Yield = the Annual Rental Income minus the Annual Expenses of the property, then divided by the Purchase Price, then multiplied by 100.

Example:

Rent: $30,000/year

Purchase Price: $600,000

Expenses: $5,000/year

Gross Yield = (30,000 - 5,000 / 600,000) × 100 = 4.17%

In a commercial property investing context, when people refer to "yield" they are often referring to net yield. Commercial property is not a focus of this website, but just something for you to note.

What is “Cash FLOW”

Cash flow is essentially the amount of money left over (or lost) each month or year after deducting all property-related expenses from the rental income; or in other words, it is a way of expressing the "Net Yield" in a dollars in/out format as opposed to a percentage.

How do you calculate it:

Monthly Cash Flow = Total Rental Income per month minus all expenses per month

Yearly Cash Flow = Total Rental Income per year minus all expenses per year

Common expenses:

Mortgage repayments (interest + principal)

Property management fees

Council rates

Insurance

Maintenance

Strata fees (if applicable)

Land tax

Example:

Annual rental income: $30,000

Annual expenses: $25,000

Positive cash flow: $30,000 − $25,000 = $5,000 profit per year

If expenses were $32,000 instead, you'd have negative cash flow (loss of $2,000)

Question:

Should you focus on achieving higher capital growth or cashflow / yield?

Answer:

Capital growth; however, they are not mutually exclusive - you need to balance cash flow / yield with capital growth if you want to build a sustainable property portfolio.

Why do we focus on Capital Growth?

Capital growth is the ultimate goal of property investing - the increase in your property's value, which will compound over time, is what will ultimately allow you to reach your passive income / financial freedom goal. Focusing on properties with strong capital growth is what will provide you with the equity you need to purchase additional properties without using your own cash reserves and will help ensure that your money outpaces inflation.

In other words, it is not the few thousand dollars you get in your pocket at the end of the year post-tax from a positively geared property which will change your life - rather it will be the hundreds of thousands (or millions) of dollars increase in the value of your properties over time which will give you and your family more financial options in the future.

Due to the high-holding costs in residential property investing, it is unlikely that focusing solely on cashflow / yield will lead you to reaching your passive income / financial freedom goal within a reasonable amount of time. This is because it will also likely lead you to investing in certain locations whose economy is dependent on a single industry, such as mining (e.g. Mount Isa, QLD), which may provide you with high rental income initially but the property prices and vacancy rates are very volatile (i.e. they have periods of rapid increases followed by significant decreases). These rental returns also typically do not improve over time as the rental growth in these areas is also very unreliable.

On the other hand, if you ignore cashflow / yield completely you won't be able to afford to hold your investment property for long periods of time without it having a significant impact on your lifestyle, financial health and borrowing capacity - you should note that the banks consider the yield of your existing and proposed property purchases when deciding how much money they will lend you.

Therefore, it is vital that you consider what a healthy cashflow / yield is for you, then ensure that you buy properties that offer the best capital growth opportunity and meet your cash flow needs.

To be crystal clear: this does not mean the property you buy needs to be positively geared (i.e. the rent is greater than the expenses) from the moment you purchase it, as the chances are very high that it will not be. The reality of property investing today is that it costs money to make money, at least initially, because if you purchase in high capital growth areas with strong rental pressure the increases in rent over time will outpace your holding costs, then eventually the property will become neutrally / positively geared.

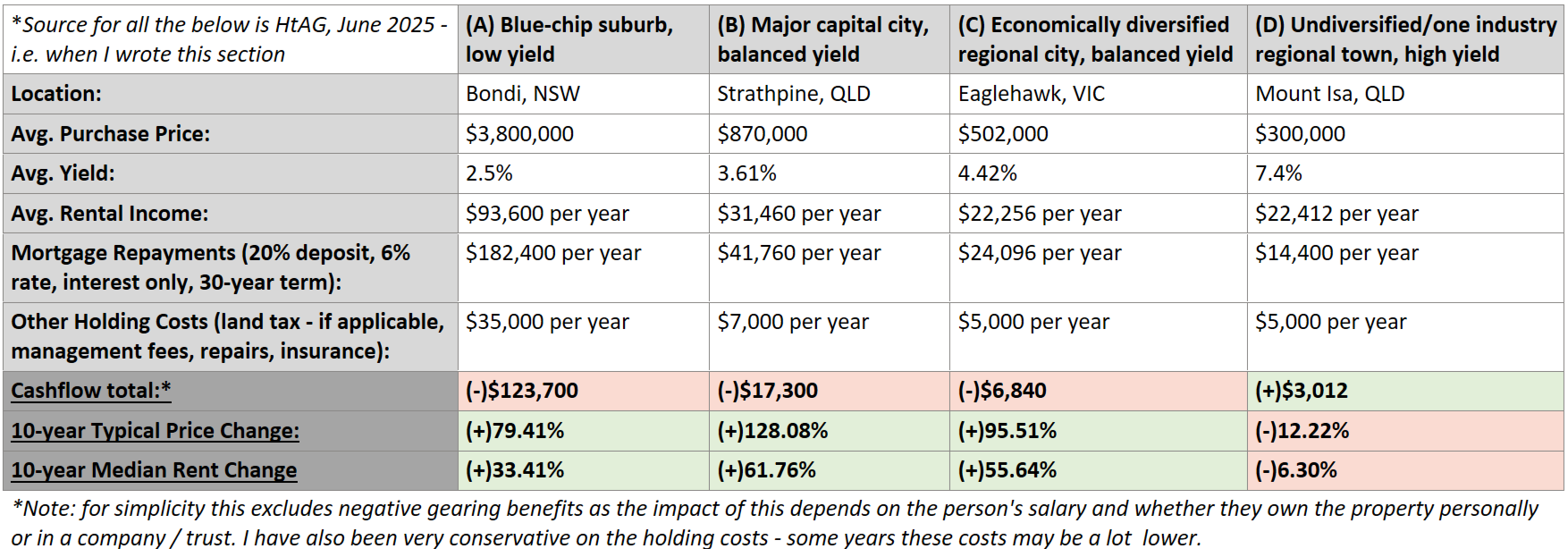

To help demonstrate the points I have raised above, I have outlined a basic analysis of some suburbs that have low yields, more balanced yields and high yields.

The above table is by no means a suggestion that you should or shouldn't buy in these areas at the time of reading this, and it is not a perfect representation of the costs / benefits of investing in these areas over the past few years (and my math might be a bit off, but oh well cut me some slack). Rather, the table aims to illustrate to you the following general concepts:

If you focused on high yield locations (i.e. Mount Isa): it may not cost you any money to hold each year; however, there is a strong possibility that you will not achieve any capital growth over the long-term and your property may decrease in value. As a side note, properties like this in locations like Mount Isa might end up being negatively geared if you can't find a tenant quickly - which is a very notable risk given the vacancy rates in these areas are volatile.

If you focused on blue-chip, low yield locations (i.e. Bondi): you may achieve notable capital growth in the long-term; however, it would also cost you a significant amount of money each year just to hold the asset, which may work for some people with extremely strong incomes but is unrealistic for the average Australian looking to build a sustainable portfolio with multiple properties. As a side note, you will see the blue-chip suburb actually grew less than the balanced yield locations - but we will talk more about the weakness of the 'blue-chip is best' argument later in this website.

If you focused on economically diverse locations with balanced yields (i.e. Strathpine and Eaglehawk): you will achieve significant capital growth in the long-term while also not incurring an unbearable amount of holding costs each year. This will help you expand your portfolio beyond just one or two properties while also living a more financially stable life. As a side note, the increase in rent in the future will also reduce holding costs over the long-term - if you buy right, the worst yield you ever have on your property will be on the day you buy it.

Just in case this is still not clear, let me demonstrate this through some different numbers so you can visualise what I mean better:

As you can see above, if you go with Property A you make $35,000 in capital growth instead of $15,000 with Property B, yes it cost you $8,000 to hold but remember that until you sell the property the gains you make it on it are tax free - i.e. you can potentially extract this amount from the bank as equity without being taxed, whereas the $3,000 you make from Property B each year will be taxed - meaning that you end up being around $20,000 better off in the first year alone with Property A.

Now let's extrapolate this out 10 years, but let's assume Property A has experience a rental growth of 60% over that period, similar to Strathpine, and Property B has a rental growth of only 10%, which is generous when you look at what happened to rents in areas like Mount Isa over the previous 10 years (i.e. they actually decreased).

Hopefully it is more obvious now that the benefits of prioritizing growth over higher yields are exemplified in the longer term - if you went with Property A you will have made $483,000 in capital growth over 10 years compared to the $172,000 in Property B - yes you will have had to pay more holding costs on Property A during this 10 year period but these costs are far outweighed by the capital growth you achieve, and after 10 years Property A will likely be at least neutrally geared and eventually it will be positively geared.

Property A won't be giving you as much cash flow as Property B, but what would you prefer - a few thousand dollars after tax each year, or hundreds of thousands more in equity which you can extract from the bank tax free to keep building your portfolio to achieve your financial goals faster? I know which one I am choosing…

Just to reiterate, the lower the yield doesn't always mean the better growth - the two are not mutually exclusive, you can achieve both sometimes; however, it is important that you ensure you are not chasing these very high yields at the sacrifice of capital growth. You want to be looking to maximize capital growth and achieving a balanced yield which allows you comfortably afford the property and keep scaling your portfolio.

In terms of action steps and figuring out what a balanced yield is for you, I suggest:

Prepare a detailed household budget - this will allow you to more clearly identify how much money you can dedicate each year to the holding costs of a property (e.g. using the earlier table, if you can spare about $10,000 a year you know you can't afford Strathpine but Eaglehawk is comfortably within your budget). There are heaps of free budgeting tools online, here is a favourite mine of from the Australian Government - https://moneysmart.gov.au/budgeting/budget-planner

Use a property cashflow calculator - this will allow you to get a great understanding of the types of properties that you can afford based on your household budget. Again, there are a lot of free ones online but this one from Suburbs Finder is a good one for beginners (just remember it doesn’t capture absolutely everything, such as land tax and buyer’s agent fees - if you decide to use one…) - https://www.suburbsfinder.com.au/investment-property-cash-flow-calculator/.

Strategise with your mortgage broker - this will allow you to plan your property purchases more strategically because if you have an investment savvy mortgage broker (which we will discuss later in Step 2), they will be able to guide you on what yields you should be aiming for on each purchase in order to maximise your borrowing capacity and purchase as many quality properties as you can.

That’s all from me on this one. I'll leave you with an analogy I have heard quite frequently on this topic which I think sums up my point perfectly:

Think of capital growth as the engine that drives your property portfolio, and cash flow / yield as the fuel that keeps the engine running. One cannot perform without the other.

I also urge you to also watch both of the following videos for further information on the capital growth vs cashflow / yield debate.