Introduction

Stop listening to your parents… Is this provocative? Sure. Is it wrong? Not really.

"Don't buy a property far from where you live, you need to be able to touch it"

"Your cousin just bought a place in [insert suburb in the city where you grew up], you should buy there"

"Just buy a unit to get your foot in the door"

"Rent money is dead money, you are just paying off someone else's mortgage"

Chances are we have all heard this well-meaning advice before, whether it's from our parents or an estranged uncle at a family gathering. Now this advice isn’t malicious; it’s just outdated, and in most circumstances, it's wrong.

I haven't written this little prelude to blame parents for the lack of property education that exists in Australia, in many ways our parents are just stand-ins for the average Australian — and most Australians have no understanding of how to invest in property strategically using data. However, almost everyone in Australia feels qualified to give property investing advice (don’t worry I understand the irony in that statement).

Why? Because most of our parents have purchased property (over 70% for those born in or before 1980) and it has "worked" for them, and by "worked" I mean they have probably held the property for over 30 years and in which time the national dwelling value in Australia has grown in the region of over 400%. It’s a story as old as time (or your parents): someone purchases a home decades ago for the same price of a second-hand 2011 Ford Focus today (i.e. my first car for anyone wondering) and sells it for millions many years later — now I am being slightly hyperbolic here but you get my point, we have heard it all before.

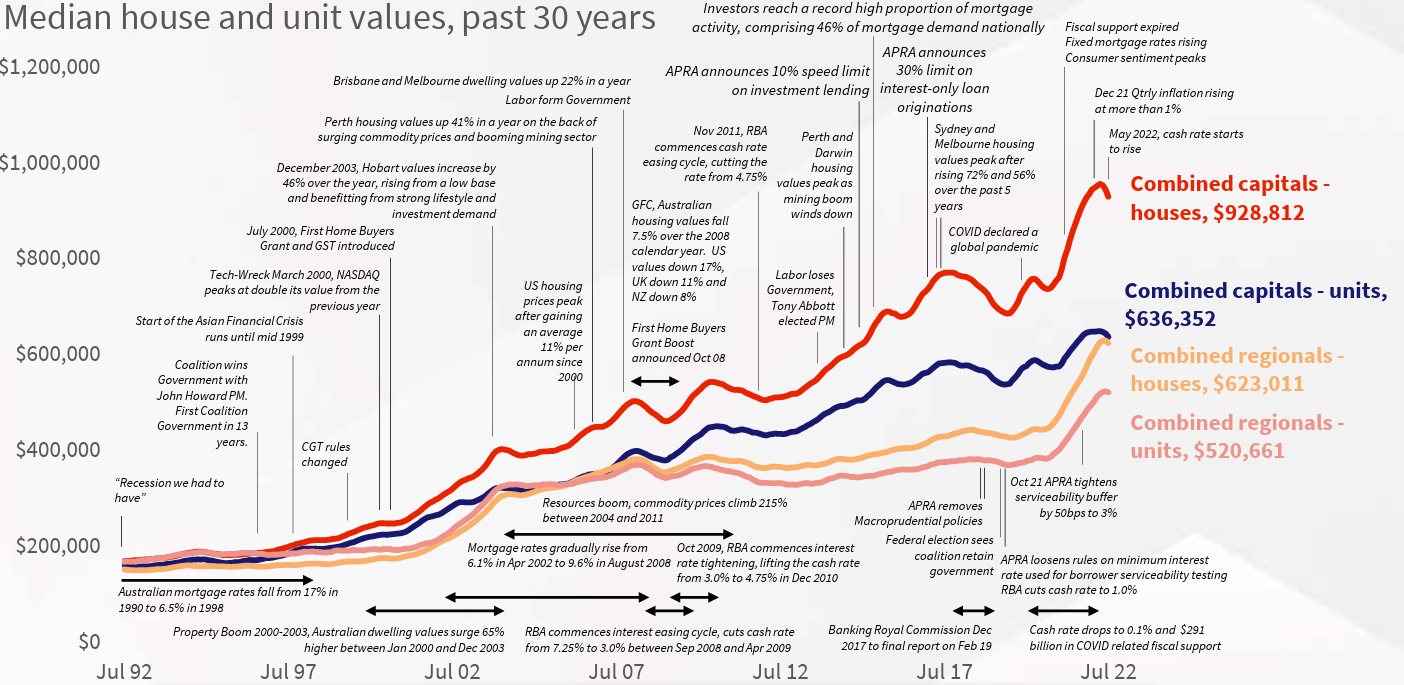

However, what all these "success" stories and historical growth rates paint over is that the Australian property market is a very cyclical market, meaning there are periods of declining prices, stagnating prices and rising prices (house prices in Australia don't always goes up?!?! Shocking I know…). In other words, if you were to map out the growth of the Australian property market on a graph, it wouldn't just be a straight line gradually increasing by the same amount each year - just take a look at this graph below from Cotality tracking Australian property values over the past 30 years if you don't believe me (the red line is the most useful one here).

It is important to note that this data is on a national level so the growth and downturn cycles (i.e. the ups and downs) are actually quite smooth here, but these cycles of increasing, decreasing and stagnating prices become even more pronounced when you look at them from a state level, city level and even suburb level - there are markets within markets in the world of Australian property.

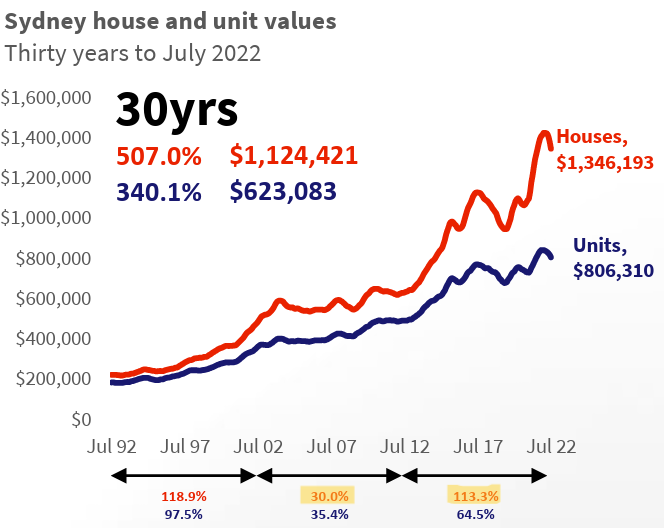

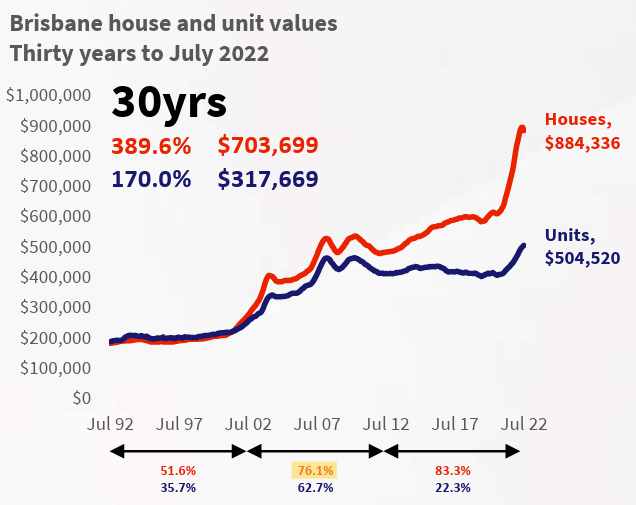

For example, what you wouldn't have heard at your family BBQ is that your uncle bought a house in Sydney in 2002 and only saw 30% growth in 10 years (which is well below the national average growth rate of 6.7% per year), in a period where places like Brisbane grew by 76% in the same 10 years.

But you would have heard all about your uncle's Sydney investment property at your first Christmas lunch post-COVID lockdown as it would have more than doubled in value through the decade right after as prices in Sydney grew over 110% between 2012 to 2022 - the below two graphs demonstrate this quite nicely (again focus on the red line - see how it isn't just a straight line going upwards!).

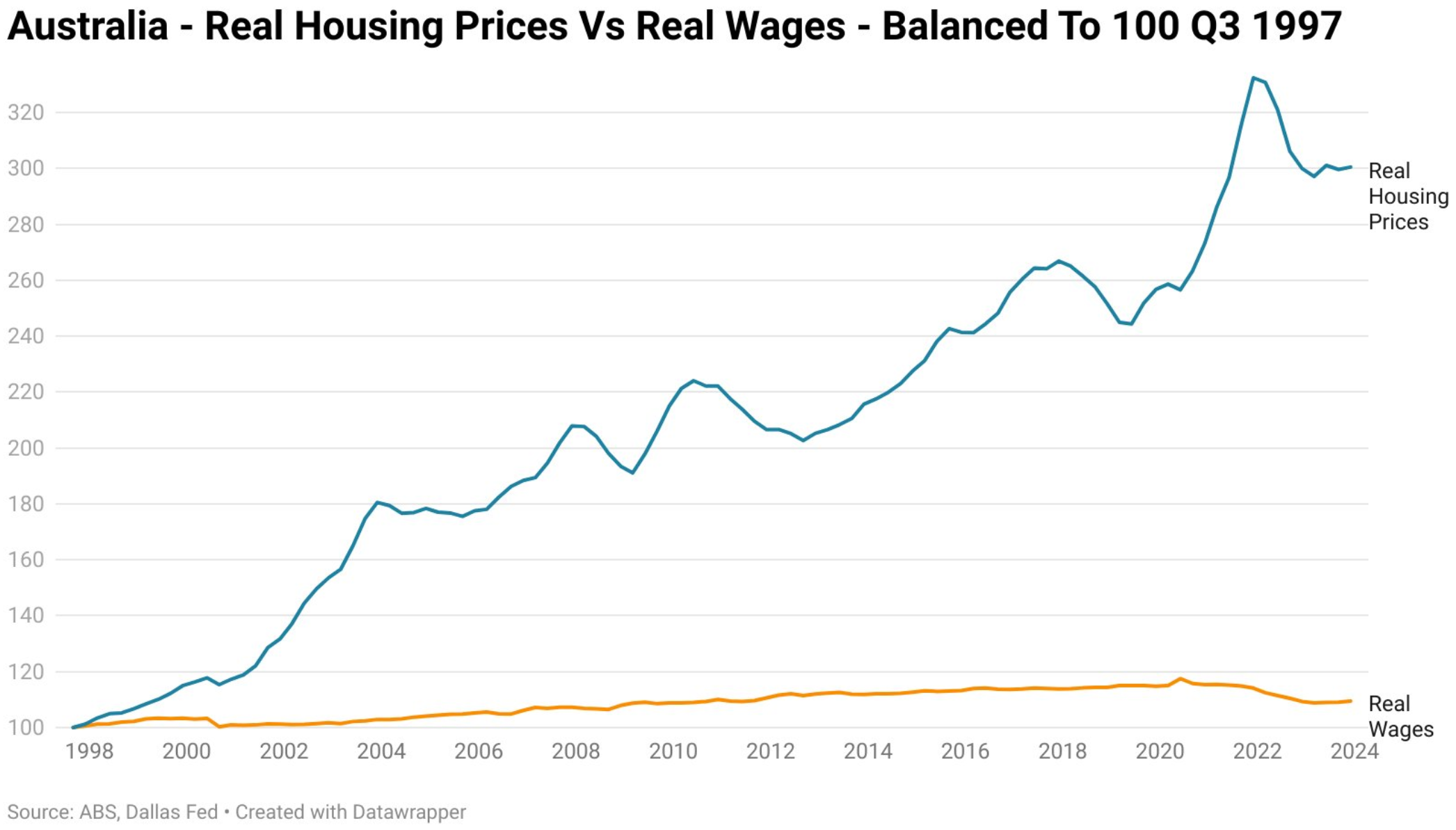

Property is a long-term game, that is undeniably true - but if you want to maximize property as a vehicle for wealth you cannot wait 4 years or more to experience notable growth - especially if it is your first property, because unless you have a very high-paying job or business, you will be relying solely on your salary to save up for the deposit on your next investment property instead of being able to use the equity (i.e. the increase in value) on your first property to fund it. Now you don't need to use a 20% deposit when purchasing an investment property, which we will discuss later, but given it takes the median-income household approximately 10.6 years to save for a 20% deposit on a median-priced home (assuming a consistent savings rate) it is not difficult to see how building a sizeable property portfolio without short term growth is almost impossible for the average Australian. This is especially true given that wage growth in Australia is significantly lower than the growth in property prices - see the below graph for reference. This shows you that property prices increase much faster than wages, meaning that you can't rely solely on your salary to build a property portfolio, instead you need to make sure you invest for the short term and the long-term.

You might be thinking "well, based on these graphs, if I just listen to my parents and buy what I can afford in the city I grew up in it will eventually increase in value over a 30 year period."

That is true, this is due to the concept of 'mean reversion' which I will touch on elsewhere but it basically means every property will have its time of growth if you hold it for long enough; however, if you want to achieve financial freedom (buzzword count: 1) from property investing there is one fundamental issue with this approach: You need short and medium term growth to scale a property portfolio.

This is especially true when you conisder that you’re paying holding costs on this property so you want it to perform sooner rather than later…

When you invest in property using data instead of 'family BBQ advice', the equity created in your first property over the first 1 - 3 years should fund the deposit for your second purchase, then the growth in your second purchase should fund your third purchase and so on, meaning you aren't relying solely on cash savings from your job but rather the increase in value of your properties - this is a slight oversimplification as you will still ultimately be restricted by the banks with respect to how much you can borrow, but hopefully you understand what I mean conceptually (this will make more sense after your read my section on equity extraction later on in Step 1).

Yes I know, this may not be what our parents have told us: “buy what is familiar and invest for the next 30 years not the next 3 years, it worked for us and it will work for you." To which I would respond with the following:

(1) short-term growth and long-term growth are not mutually exclusive - you can achieve both; and

(2) comparing the time when our parents started investing in property with today’s conditions is like comparing apples and oranges - both are fruits but they are completely different. In fact, I would go as far as to say….

Property investing is more difficult now than it was for our parents…

Rental yields are more compressed as a result of significantly higher property prices and rising holding costs.

In particular the average yield for a residential property investment in the early 2000s was anywhere from 5% - 7%, but this now sits at 3% - 4%. Obviously this varies from market to market, but the crux of the point is - almost every market in Australia has seen a noticeable decrease in yields across the board.

The following holding costs (amongst others) have also increased dramatically:

(1) Interest rates

This may be less relevant / accurate depending on the time you are reading this, but since the all-time lows of 2020, interest rates have increased significantly to around 6% depending on the bank / product.

Now before the 'Boomers' persecute me, I know that this is more or less on par with the average interest rate of the 2000s and much less than the 1990s where the average was 9-12%; but, this point is moot / invalid when you consider that the higher interest rates of previous generations were being multiplied against a significantly lower mortgage amount.

Don’t believe me? The average mortgage in 1990 was $70,000, in 2000 it was $150,000 and in 2024…..$650,000. I will leave you to do the math, but for the lazy people - that’s an 800% increase between 1990 and 2025, then 200% between 2000 and 2025. I shouldn't have to say it again, but I will just to reinforce the point, wages have not grown anywhere near the same rate.

(2) Insurance costs

With inflation and the rising amount of natural disasters being experienced in Australia as a result of climate change (going to trigger a few skeptics with that one), landlord related insurances have also increased upwards of 20-50% over the years.

(3) Maintenance costs

Particularly since COVID, general repair costs have also skyrocketed with the industry experiencing 8.5% growth in 2024 alone with projections suggesting it will grow a further 8.5% over the next 5 years.

The above is not even close to all the factors to consider in the rising holding costs of property - increasing land tax and regulation (i.e. rental caps) to name a few I haven’t mentioned, but hopefully you get the gist by now: holding an investment property is the most expensive it's ever been.

DIFFERENCE

The price-to-income ratio for the average house in Australia has increased to 8.0 from 3.0 over the past 30 years.

This is exemplified for those living in capital cities such as Sydney (12.0), Brisbane (11.0) and Melbourne (10.0).

As a result, servicing a new mortgage on a median-priced home requires about 50.6% of a median household's income, up from a 20-year average of 36.6%.

The lending environment is significantly stricter today than it was in previous years. In particular, the lending environment started tightening in 2014 and became much stricter after 2017, especially post-Royal Commission.

Generally speaking, pre-2014 you could borrow in excess of 8x your income and on much more favourable terms (i.e. lower deposit, longer interest-only periods etc.), but post-2018 it sits around 5x your income with larger buffers and more scrutiny being placed on income / expenses.

Now that statement is going to get some of the old school property gurus and commentators all fired up - but unfortunately for them, if you are capable of reading at a sixth-grade level and have some degree of integrity or objectivity (which I can confirm only a select few of them possess) you will be able to acknowledge that, on balance, this is a factual statement.

Anyone trying to tell you otherwise is most likely trying to sell you something or suffering from a mild case of the "bootstrap fallacy" - i.e. the idea that "I did it, so you can do it too" without recognizing the different starting points amongst individuals and generations. The tendency for some persons (usually in older generations, but not always) to insist that it was just as difficult to invest in property when they started still baffles me, not only because it is devoid of truth, but because they become so defensive and emotional as if the reality of today's generation somehow diminishes their own achievements.

There is no doubt some people intend it this way, but not me, good on you for taking action and investing, it was / is the smart thing to do - that is a fact, but it is important to remember that at the time I am writing this website each of the following is also a fact:

IMPACT

Your money today does not go as far in the property market than it would have when your parents were your age - i.e. you are not getting as much bang for your buck.

Meaning that if you were to blindly listen to your parents without first educating yourself and just buy what you can 'afford' in the city / suburb you were raised in, just like they did, there is a high chance you will be buying an inferior asset.

In other words, whilst your parents may have been able to buy a solid brick home on a 650m2 block in the inner suburbs of Sydney, you may only be able to afford a 1-bedroom apartment in a complex of 40 units in the same suburb or a house-and-land package with a 250m2 block in the middle of woop-woop - both of which, as I will explain on this website, are horrible investments in my humble (unprofessional) opinion.

If you are uneducated in property investing, it is harder to scale a property portfolio today than it was for previous generations.

You may have heard the stories about your parents' friend who amassed a 10+ property portfolio from just buying houses in-and-around Sydney in suburbs they could afford at the time, all whilst working a job that is not too dissimilar to yours.

I don't think I am going out on too much of a whim here by saying that is now unrealistic. To achieve a similar result today's generation needs to: (1) earn more; and (2), most importantly, make smarter / well-informed purchases - because if you don't educate yourself and purchase a dud property based on 'family BBQ advice' there is no guarantee the banks will lend you more money to buy another property any time soon, which will hinder your ability to build your property portfolio.

The financial consequences and opportunity cost of purchasing a dud property is far higher today than it was previously.

Chances are that if you are buying a property today, especially in a capital city, the expenses will be greater than the rent that it brings in - i.e. the property costs money to hold, or in other words, it is negatively geared.

In principle, that is perfectly fine and to be expected, because the reason we invest in residential property is for the capital growth not the rental income (and not the tax benefits… I will explain this further elsewhere on this website).

However, if you are not educated, and the property you purchased does not grow in value because you took investing advice from your parents, then you are spending a larger amount of money to hold an asset than your parents may have and the cost of you holding this dud investment until it finally has its time in the sun (I am referring to mean reversion here again) may be crippling to your financial health, lifestyle and the scalability of your portfolio.

Now I wouldn't blame you if you read the above and thought one or both of following things:

(1) I thought this website was supposed to help me invest in property, not turn me off it completely; and

(2) all this guy does is complain about how much harder it is to invest in property today.

Whilst the latter definitely has some truth to it, the intention of highlighting the differences between someone starting their investment journey today versus those who may have started it many years ago was not to scare you from property investing or to make you vindictive against your parents (for the record, I love mine very much), but it was to show you that whilst the asset we are all taking about is the same, the investing landscape today is very different and as Morgan Housel once said:

"Beware of taking financial cues from people playing a different game than you are."

Generating wealth from property investing in Australia is without-a-doubt still possible in today's generation - people are doing it every day, including myself. In fact, whilst the downsides of property investing are much more prevalent today, I would argue the upsides are just as good, if not better. Just take a look at those who invested in Perth, Townsville or Brisbane back in 2021 - 2023: they are all up anywhere from 50% - 100% in the matter of a few years. Yes, I am sure plenty of these people took the advice of their parents and just bought a home in the city they grew up in, and good on them - but that is not investing, that is gambling. How do I know? Because at the same time there was thousands of people listening to their parents and buying in Melbourne who had their homes decrease in value during the course of 2021 - 2023 (hope they didn't sell… as it looks like Melbourne is primed for some capital growth as I am writing this).

So how did these people know with confidence that they should invest in areas like Perth, Townsville, Brisbane etc. in 2021 - 2023? Were they just lucky? Did they hear about it in the news? Are they geniuses? As one of these said people, I can assure you none of those are correct (especially the latter). They used data.

One advantage we do have over our parents in the property investing game is resources. Whilst our parents were looking at the back of newspapers for properties to buy we now have access to listings from all over Australia and more data than we could ever need to analyze property markets and make the best investment decisions. It took me a while to get here, but that is more or less the point of this website, directing you on the path to stop taking your parents' approach to property investing and instead take a data-driven approach (buzzword count: 2) - because the truth is: