Step 1 - Understanding the Fundamentals

What is equity?

Equity is simply the current market value of your property minus the amount of money you owe on the loan for the property.

i.e. Equity = Market Value - Loan Balance

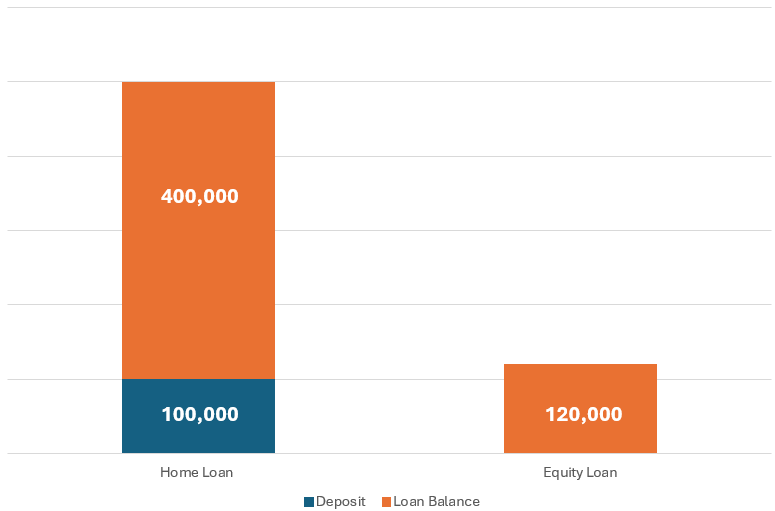

By way of example, let's say you purchased a home for $500,000 and you used a 20% deposit ($100,000) which makes your loan amount $400,000. Fast-forward 1 year and because you have read my website from top-to-bottom your property has increased in value to $650,000.

Market Value = $650,000

Loan Balance = $400,000*

Equity = $250,000

*Note: this assumes that you are in the interest-only period of your mortgage, if you have opted for principal and interest then the loan balance would be lower. I have done a separate section on interest-only vs principal and interest in Step 2 where we discussed Mortgage Brokers.

Now here is where it gets interesting, the bank will actually let you access some of this equity - and by access I mean let you take out a new loan. However, just because you have $250,000 in equity doesn't mean that the amount of this new loan will also be $250,000, there is a difference between 'equity' and what the banks consider to be 'usable equity'

‘Usable’ equity and LVRs

Usable equity is the portion of your equity that a bank will actually allow you to access based on that bank's specific maximum loan-to-value ratio (LVR) policy.

LVR is the percentage of a property's value that you are borrowing and it is calculated as follows: Loan Balance divided by Market Value multiplied by 100

i.e. LVR = (Loan Balance / Property Value) x 100

Let's use the numbers in our above scenario as an example:

400,000 (Loan Balance) divided by 650,000 (Market Value) = 0.62

0.62 multiplied by 100 = 62%

Therefore, the LVR of the property in our above scenario is 62%.

In Australia, most banks will let you borrow up to 80% of the property value (i.e. 80% LVR) without paying Lender's Mortgage Insurance (LMI), or up to 90% of the property value if you are happy to pay LMI (this can differ depending on your occupation).

I have done a separate section on what LMI is and whether you should consider paying it or not (see Step 2 where we discussed Mortgage Brokers), but for argument's sake, let's calculate our useable equity using the 80% LVR route. The calculation for which is as follows:

Usable equity = (Market Value x Max LVR %) - Loan Balance

650,000 (i.e. Market Value) multiplied by 80% (i.e. Max LVR) = 520,000

520,000 - 400,000 (i.e. Loan Balance) = 120,000

Therefore the useable equity in our above scenario is $120,000. However, it is important to remember that you also need to have the borrowing capacity in order to take out an equity loan - if a bank doesn't believe you can afford to borrow any more money it ultimately will not matter how much equity you have.

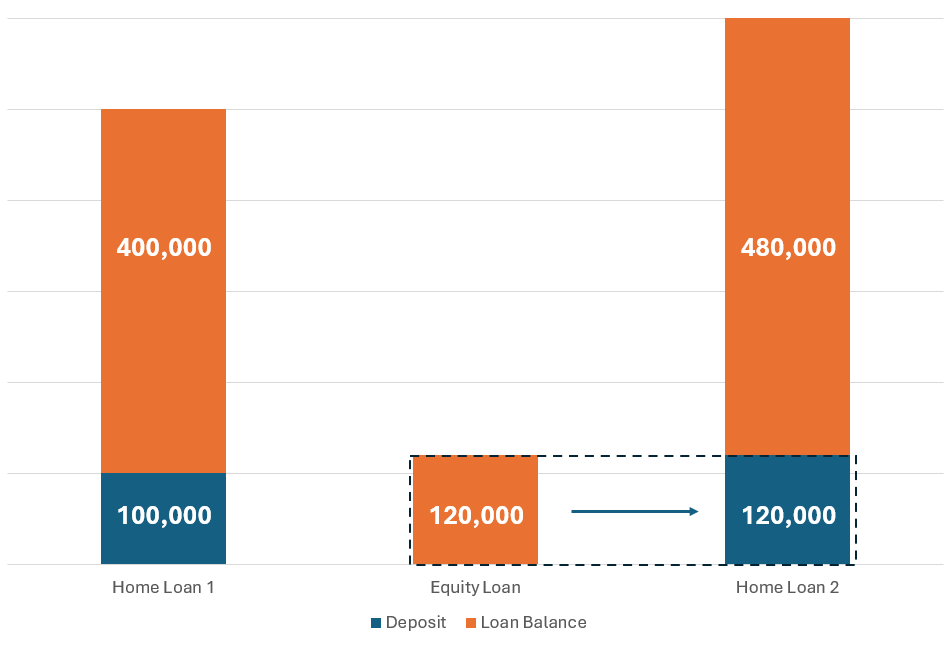

Assuming we have talked to our mortgage broker and they have advised us we have sufficient borrowing capacity, we then go to the bank and extract the useable equity. This then leaves us with the loan balances outlined in the below chart:

Pop quiz: What is the LVR on the second investment property

(i.e. Home Loan 2 - $600,000 market value, 20% deposit funded by an equity loan)?

(a) 80% LVR; or

(b) 100% LVR.

Answer: The answer is (b) - this is bit of a trick question, so don't worry if you got this wrong.

The difference here is that unlike the first property where cash was used for the entire 20% deposit, here we used money from our equity loan - i.e. borrowed money.

This means that we funded the entire purchase using the bank's money and none of our own so the LVR is technically 100%.

Technically, you can go and spend the money you get from the equity loan on whatever you want.

However, I want to assume that because you are invested enough to be reading this website, you are also smart enough to not go and waste this money on a new Ford Raptor or European holiday (pick your poison).

Instead, what we are going to do is use this $120,000 from the bank as a deposit for our next investment property (you could also use the equity to cover things such as stamp duty, legal fees, buyer’s agent fees etc. if you have enough - otherwise you will need to add some cash savings into the mix).

For example, let's say we do exactly that and purchase a second property worth $600,000 using our $120,000 equity loan as the 20% deposit - this then leaves us with the loan balances outlined in the chart below:

Now please (I am begging you) remember that an equity loan is not free money - it is like all other loans, it has an interest rate attached to it and you need to make repayments on it. So when you are calculating your cash flow for your next property and you are using equity, make sure you consider the repayments on this equity loan into your total holding costs calculation.

Sorry if I burst some people's bubble with that fact, but remember using equity loans is still the most efficient way of scaling a property portfolio because ultimately you will be able accumulate equity in a property for a deposit much faster than you will be able to from just relying on your savings (assuming you have purchased in the right area at the right time) because:

You don't pay tax on equity, but you do on your savings (through income tax); and

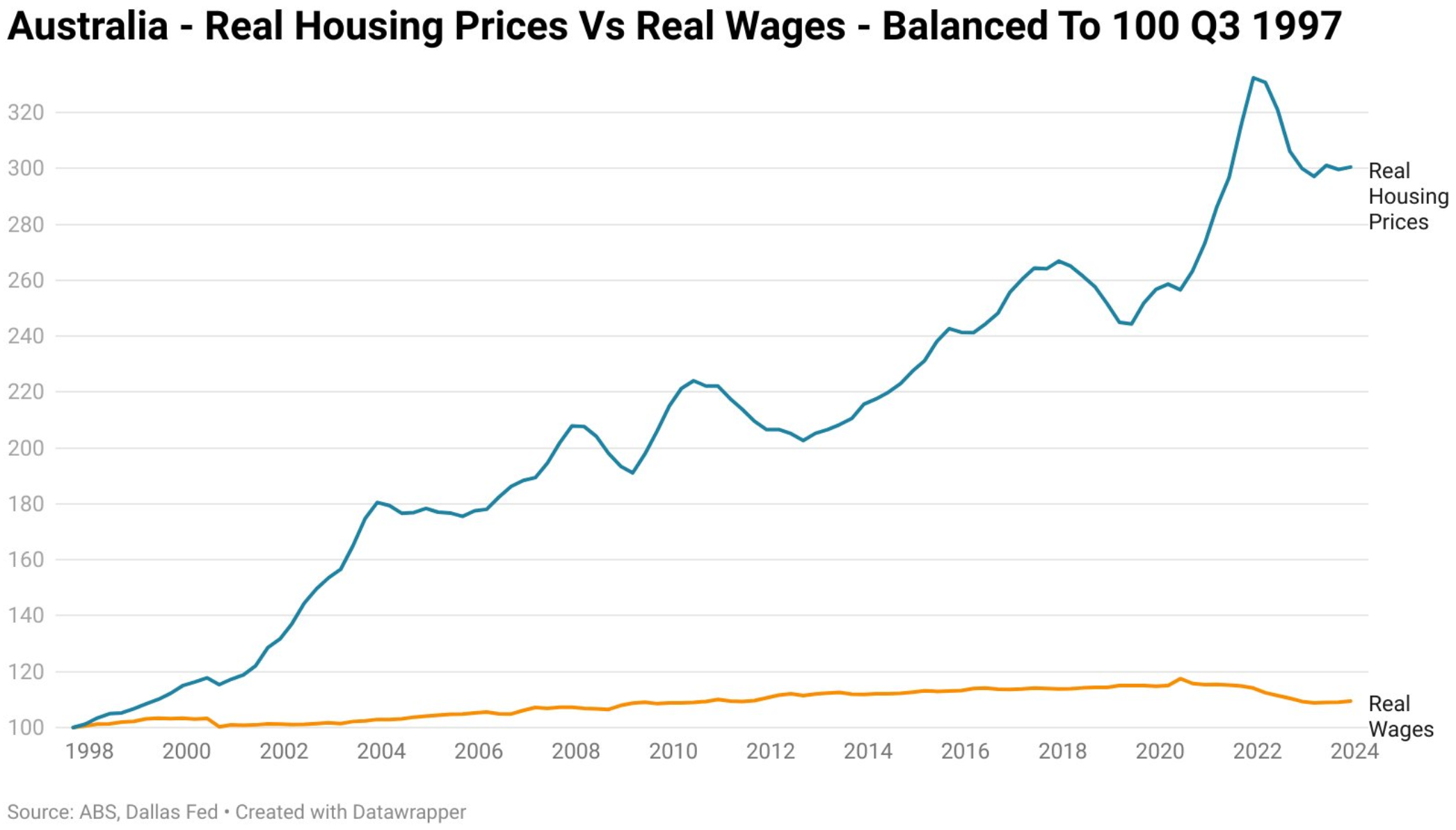

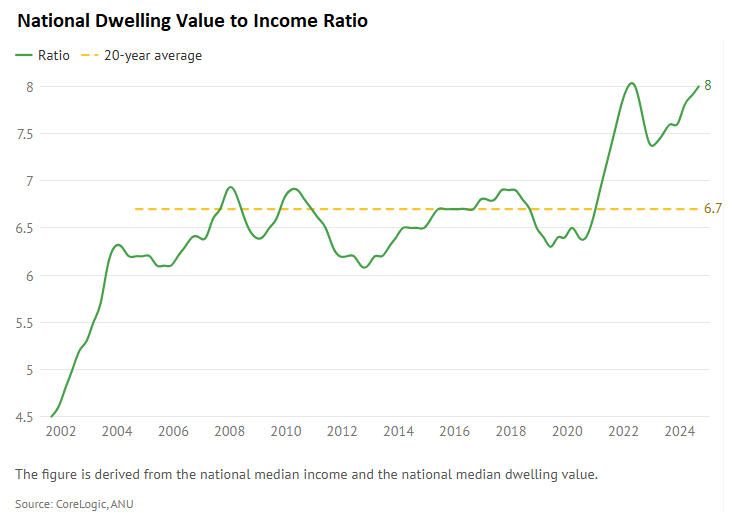

House prices have grown / are growing at a much faster rate than wages in Australia.

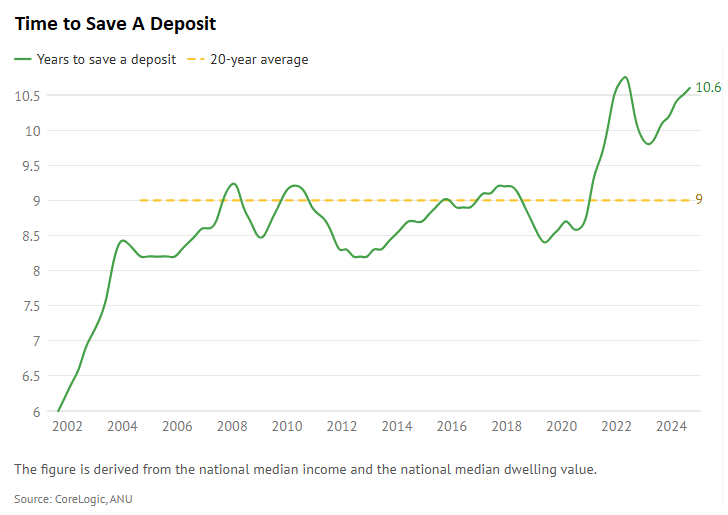

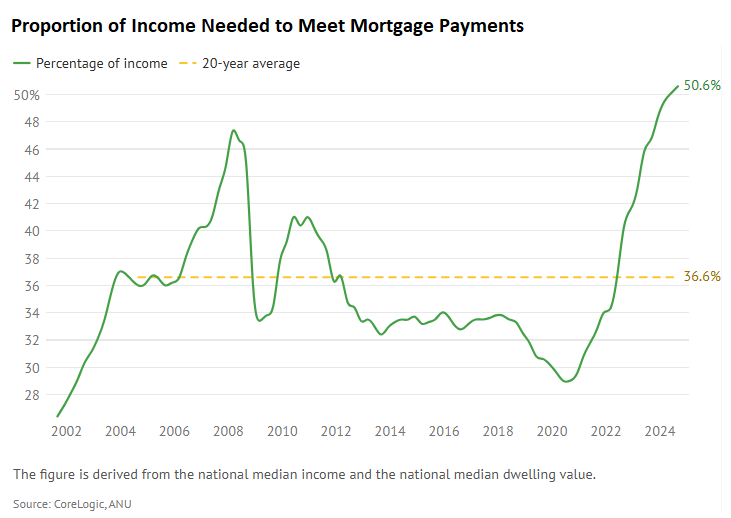

I have shown you variations of these graphs before on this website, but just to reinforce my second point take a look at the below. The two graphs on the top row, whilst depressing every time I see them, probably illustrates my point the best.

Here are a few useful videos which you may want to watch if you want to double-check you have understood everything I have said above, or if the above is confusing then perhaps these videos explain it better (feel free to give the topic a search on YouTube also - heaps of videos out there explaining this concept).

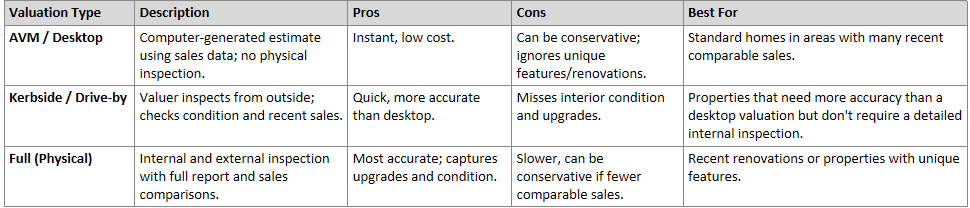

Bank Valuations

The first is 'bank valuations' - you will have seen above that the 'market value' of your property is a major factor in determining how much equity you can extract. Now market value in the context of equity extraction will be based on the result of the valuation undertaken by the banks and can be managed by your mortgage broker (i.e. you don't need to go order one yourself or talk to the bank directly) - it is not based on whatever a real estate agent might have told you.

For reference, just because you have a bank valuation for $X it doesn’t actually mean that your property with sell for that amount - the true market value of your property is only established once it is sold. Bank valuations can also vary significantly, with some banks being known for giving higher bank valuations and others known for being more conserative. So whenever you see a buyers’ agent posting bank valuations on social media, remember to take them with a grain of salt…

There are also a few different types of bank valuations - each with their own pros and cons.

Extracting Equity from your PPOR

Secondly, remember that you don’t only have to extract equity from investment properties, you can also extract equity from your principal place of residence (i.e. any house you have bought to live in yourself). So if you haven't recently, go and ask your mortgage broker for a bank valuation on the family home so you can assess your options.

Nothing else from me on this, a nice short and sharp one to finish this section off - time to move on to the next fundamental.