Step 1 - Understanding the Fundamentals

"Buy the worst house on the best street"

This is something we have probably all heard at a family gathering before and as you know by now, I am not a fan of your parents' property advice; however, albeit unintentional, there is actually a nugget of investing gold here (if you dig really, really deep) – the house you are buying is not as important as the land it sits on.

Now that is probably too generous of an interpretation of the true meaning behind that quote, but I digress.

Here is the key point for you to understand: the land that the house sits on is what actually goes up in value over time, not the house itself (no matter how new and fancy it is).

So why does land appreciate and houses depreciate?

It goes back to the concept of supply and demand we discussed earlier - land is limited and can't be increased. The amount of land you see around you today is the amount there will be until the end of time. It is this scarcity, combined with demand, which makes the value of land increase over time.

The same cannot be said for houses. Since they are physical structures, they deteriorate over time (i.e. due to weather, use, aging etc.) and they can become more outdated as building standards and design preferences changes (all the old 'ugly' houses you see today were new and shiny at one point, and the same thing will happen in 30 years' time to the houses built today…if they last that long). Houses can also be built and replaced as needed, but you can't just go and create more land.

Let me try explain this using my favourite real estate game:

How much did this sh*t box sell for?

House and Land Myth

105 Haig Road, Auchenflower, Qld 4006

Land Size: 339m2

Sold Price: $1,400,000

Date Sold: 19 September 2024

23 Margate Avenue, Frankston, Vic 3199

Land Size: 1,620m2

Sold Price: $1,600,000

Date Sold: 29 April 2025

As you can see above, despite the houses on the right being far nicer and in the same area, the dilapidated homes on the left all sold for more (in most cases, significantly more) – this is because they had a larger land size. I was not just cherry picking homes either, I could provide countless more examples. Think of a new house in the same way that you think of a new car, yes it is nice and shiny (and expensive…), but from the moment you pick up the keys it begins to depreciate in value.

Size doesn't always matter… it's about value

So does this mean you should just go buy a massive plot of land in the middle of nowhere and sit on it for 30 years? Well no… the value in land is attributed to its scarcity - meaning it is not strictly about the size of the land, but rather its value. Think of it this way: take a look at the below parcels of land - one is only 151m2 and is located in an area with limited land supply (i.e. Rose Bay, NSW), and the other is 875m2 but is located in an area with plenty of land supply (i.e. Mickleham, VIC). Now take a look at the price difference…

The property will get tenanted very easily because it's new and they are offering me a 1-year rental guarantee anyway in case I can't find a tenant.

The property will have strong capital growth because it is new and is located in a "growth corridor"

Buying a brand new house is a good investment decision because I will get money back at tax time due to the depreciation benefits.

The property will have less maintenance costs because it is a brand new property.

216/9 The Arcade, Docklands VIC 3008

Initial Purchase Price (2009): $582,000

Recent Sold Price (2025): $530,000

Total Loss = $52,000 (excl. acquisition costs, holding costs, selling costs and opportunity cost - aka. a lot more money)

What you need to do is ensure that you are purchasing a property with a high land-to-asset ratio. Or in other words, you want the majority (at least 50%) of your property's total value to be attributed to the land itself as opposed to the home built on it. We will get into how to calculate the land-to-asset ratio later on in this website in Step 5 when we go through the property selection criteria – but as a very, very general rule I personally wouldn't be buying houses on less than 450m2, but please remember it's about the value of the land, not its size. So depending on how expensive land is in the suburb you are investing in and the price you are paying, it may be entirely appropriate for you to be purchasing a block smaller than 450m2.

To summarise this into one key takeaway: once you have decided what suburb you want to invest in, you want to be buying established / older homes on larger blocks of land in that suburb, as opposed to the new homes on smaller blocks of land. This will ensure that most of the purchase price you have paid is attributed to the value of the land instead of the house (i.e. this will give you a higher land-to-asset ratio).

"But my [accountant / mortgage broker / buyer's agent] told me I shouldn't buy an established house and instead I should buy a brand new 'house and land' package from this developer because then I can get all this money back in tax from the depreciation?"

I am sorry to say this, but whoever gave you that advice is either: (1) too stupid to understand the mistake you are about to make; or (2) thinks you are too stupid to know better and is trying to make a quick buck out of you (unfortunately, it is usually the latter).

New vs Established Homes

If you found your way on to this website, then there is a good chance that you have seen an advertisement pop up on your social media trying to sell you the dream of retiring from your 9-to-5 job in just a few years through purchasing a 'house and land' package (and if you haven't yet, you probably will now).

"The property we build for you will be located in a growth corridor and there is going to be huge population growth here."

"You will get great tax depreciation benefits each year."

"It will be really easy to get tenants because it’s a new property - we will even give you a rental guarantee for a year."

"This property will be brand new so you won't have to worry about maintenance issues."

These are just some of the common sales tactics that these grifters will use, and if you hear any of these buzzwords from someone - whether that be your accountant, mortgage broker, buyer's agent, property advisor or whoever - you need to run away as fast as you can. I don't care if someone in your family recommended them or you just attended a seminar / webinar and they seemed like really genuine people - 99% of the time these people are not operating in your best interests as they are just trying to secure their commission.

You didn't know they were getting paid under the table? Well, that doesn't surprise me as these people are not very forthcoming about it. Anyone that is pushing house and land packages to you is often getting anywhere from $30,000 - $60,000 in commission from the developer… and where do you think this money is coming from? Do you think the developer will just take that off their profits? Absolutely not, the margins are already very slim in property development these days, this commission is coming straight from your wallet because it is baked into the purchase price of the house and land package.

Remember those bank valuations we talked about before? The reality is that for many people who fall into the "house and land package" trap these days, the bank valuations they get from the bank at the time of settlement are significantly below the price they paid due to all the hidden costs and commissions which are baked into the price that they paid the developer.

Let me give a little example using some numbers: let's say you paid $850,000 for a house and land package - you would hope the market value is at least $850,000 right? Wrong - lets break it down further to see what you are really paying for:

minus $50,000 in commission fees;

minus $30,000 for the rental guarantee;

minus $20,000 or so for ad hoc things / a bit extra off the top for the developer to boost their margins.

All of a sudden your house is actually only worth $750,000, which is what the bank valuation will say also, meaning you overpaid by $100,000. But surely the supposed benefits you get from a new house and land package (e.g. capital growth and tax depreciation) will outweigh this cost? Unfortunately, that is very unlikely… let me explain:

Investing Reality

Saying an area is a "growth corridor" is like trying to polish a turd: you can try all you want but it's still a piece of sh*t.

House and land packages are generally only offered in greenfield estates where there is an abundance of land and therefore no scarcity for houses - which means supply tends to outweigh demand in these areas for many years, which as you now know means that house prices don't grow very much (if at all). For reference, go back and take a look at the picture of that block of land in Mickleham which I shared further up on this page - that is a house and land estate.

Additionally, the land-to-asset ratio on house and land packages is usually very low. This is because these days the blocks tend to be quite small (anywhere from 200m2 to 400m2), and because the land is not scarce, it is not worth very much but the house is brand new so it is very expensive - meaning that well over 50% of the price you paid can be attributed to the value of the house instead of the land, which is another reason these investments tend to perform very poorly in comparison to established houses on larger blocks.

Will a house and land package experience some capital growth in the next 30 years? Probably, but that's because all properties get their time of growth eventually - think back to when we talked about mean reversion. However, as we have discussed many times, you need to experience capital growth in the short / medium term if you want to build a property portfolio, you can't be waiting 10+ years which will likely be the case with house and land packages.

Investing for tax benefits is not a property investing strategy - it just isn't.

Depreciation is an ancillary benefit (i.e. a bonus). It will not get you any further to financial freedom because ultimately what we need is capital growth and sacrificing that so you can get a few thousand dollars from the tax man does not add up from an investment perspective. You can also get depreciation on certain established properties (depending on when they were built and if you have done any renovations) so this is not a benefit that is unique to house and land packages.

It is also vital that you understand that you will need to repay anywhere from 45-50% of the depreciation you claim (confirm these amounts with an accountant as they may change over time) to the ATO when you sell the property one day - it is not all free money. This lump sum bill can be quite substantial depending on how much depreciation you claim over the years (I am talking like easily over $40,000) which can catch a lot of investors by surprise.

Unfortunately, this couldn't be further from the truth and the proof is in the data. Most areas where house and land packages are built have vacancy rates well above the national average of 1.2% (July 2025). Looking at Mickleham again for example, its vacancy rate as at July 2025 is approx. 5%, with its neighbouring suburbs that are also house and land estates having vacancy rates of approx. 10% (Donnybrook and Kalkallo). For reference, 3% is considered a balanced vacancy rate. Ultimately, this means you are going to find it very difficult to find a tenant.

There are a few reasons for this, one being that generally speaking these areas are not very attractive to renters due to the lack of infrastructure (such as public transport, roads, schools etc.) and the other is that these areas are often dominated by investors which means that renters that do want to live in the area have various options to choose from (and given most house and land packages tend to look the same, there isn't much differentiating each house).

"But the developer said they would guarantee my rental income for 1 year!" - this is yet another dodgy sales tactic.

Firstly, as we have established above, this rental guarantee is not free - you have already paid for it in the purchase price. Secondly, what do you think will happen as soon as the rental guarantee is over - will it all of sudden be easier to find a tenant? Nope - you will be in the exact same situation you were in a year ago, struggling to find a tenant. Just remember that these developers are here to make money off you - they are not your friend, so ask yourself why would they offer a rental guarantee if there was going to be no issues with renting the property?

If I was writing this 10 years ago I would have had to agree with this statement, as it is generally true that newer properties have less maintenance costs than established / older properties. However, there has been a significant decrease in the quality of new build homes over recent years, most likely due to the increase in construction costs, in which the cost of rectifying major defects far outweighs the maintenance costs of older homes. For example, they have done quite a bit of research into this in NSW in which the NSW Building Commissioner recently found that almost one in two freestanding homes that have been built in the past year have had major defects (noting I am writing this in late 2025…).

If you want more evidence of Australia's declining building standards, just go watch my favourite YouTube creator @SiteInspections.

Now let's say you get lucky and sign up with a great builder, so your maintenance costs are ultimately lower than an older property. The capital growth that you will experience from purchasing an established property on a larger block will far outweigh any difference in maintenance costs… it shouldn't even be close (if you pick the right suburb, that is). This means that you will have sacrificed hundreds of thousands of dollars in growth as well as the security of having a lower vacancy rate (i.e. so more consistent rental income) all so you could save a few thousand dollars in maintenance costs… I don't know about you but that doesn't sound worth it to me.

Here are a few useful YouTube videos if you want to learn more / if what I have said above makes no sense.

Houses vs Units

So by now you understand that ultimately it is the land that grows in value, but what does that mean for apartments? Does this mean apartments are bad investments and we should just be investing in houses?

You have just opened up one of the biggest cans of worms in property investing: the houses vs units debate.

It really isn't too much of a debate in my opinion - you should almost always be investing in houses instead of units (especially if you are new to property investing). Why? Because they almost always perform better than units. In fact, the national average growth rate for houses over the past 25 years was 6.8%, whereas for units it was 5.9% - this has translated to a 412% increase in median houses prices compared to a 316% increase for units.

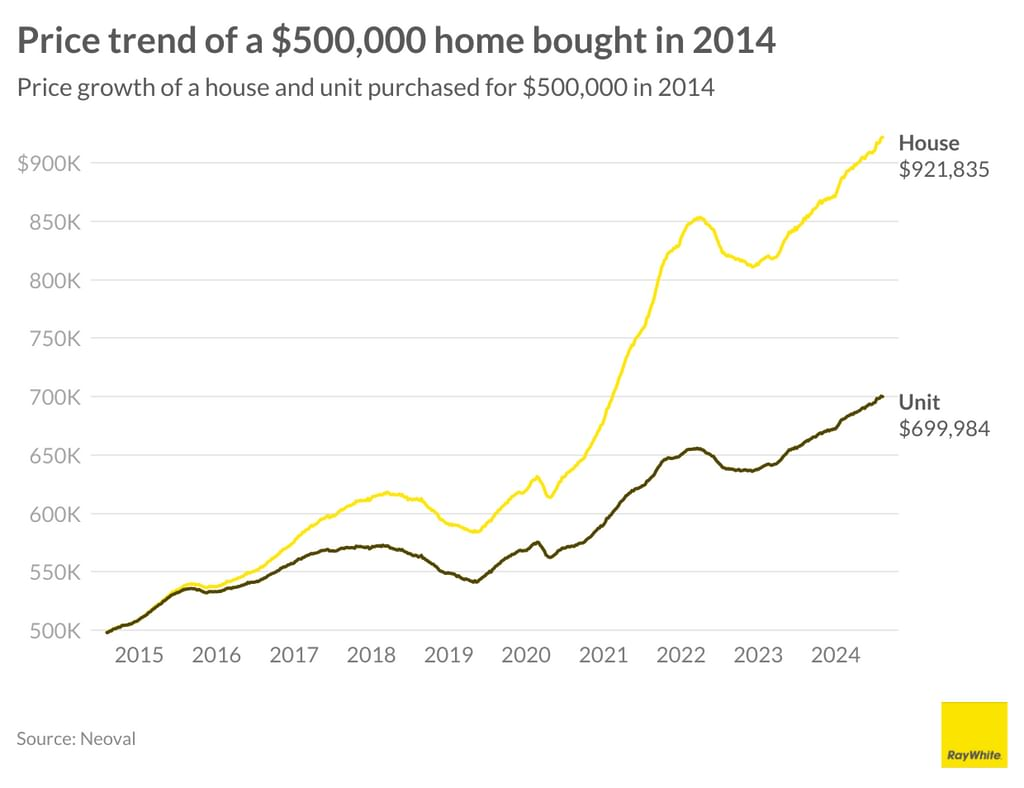

The economists over at Ray White conducted an interesting study recently which compared the performance of houses vs units if they were both bought for $500,000 at the same time in 2014. As you can tell from the below graphs, houses were the clear winner at a national and state level - and for the record, it is a similiar story for when you do the same test across a longer time period (e.g. 20 years+, 30 years+).

So why do houses tend to outperform houses over an extended period of time? Because houses have a larger land component - i.e. exactly what we talked about above, land is what appreciates in value and since houses have significantly more of it that means they will perform better in the long term

As a result of their larger land size, houses are also much more scarce than units - as we have said before, you cannot just create more land, what you see today is what you get; however, there is unlimited sky which means that, subject to zoning, developers will be able to continue spawning units in high to medium density areas for the foreseeable future. There is therefore also a greater supply side risk when it comes to investing in units which can put downward pressure on prices.

This is something which catches out a lot of newbie investors - they think are buying a unit in a great location because it is perhaps close to a train station or the CBD, but what they haven't realized is that these not knowing that these types of areas are also where the zoning is more likely to allow for massive apartment complexes to be built and before they know it another 200 units have been developed next door which ultimately increases supply in the area and results in the price of their investment stagnating / decreasing.

Take a look at the below units for example.

2407/7 Australia Avenue, Sydney Olympic Park, NSW 2127

Initial Purchase Price (2014): $629,000

Recent Sold Price (2025): $545,000

Total Loss = $84,000 (excl. acquisition costs, holding costs, selling costs and opportunity cost - aka. a lot more money)

Please remember the emphasis on the right type of townhouses. Similar to what we discussed with units, I will go through what to look for in a townhouse in the property selection criteria section of this website, but again you generally want to be targeting basic brick townhouses that have low body corporate fees (if you can get a freehold one, even better) and in small complexes of 4 - 12 so you are maximizing the amount of land you are purchasing.

For those interested, here is a YouTube video on the townhouse market in Australia.

I have done this little section on townhouses as they are a superior asset class to units and I believe townhouse investment will become increasingly more relevant in the future as affordability weakens in Australia - especially for those with established property portfolios who maybe have a few houses around Australia but don't have the capacity to break into the freestanding housing markets of the major capital cities. But let me be clear: houses are by far the better asset class and it's not even close.

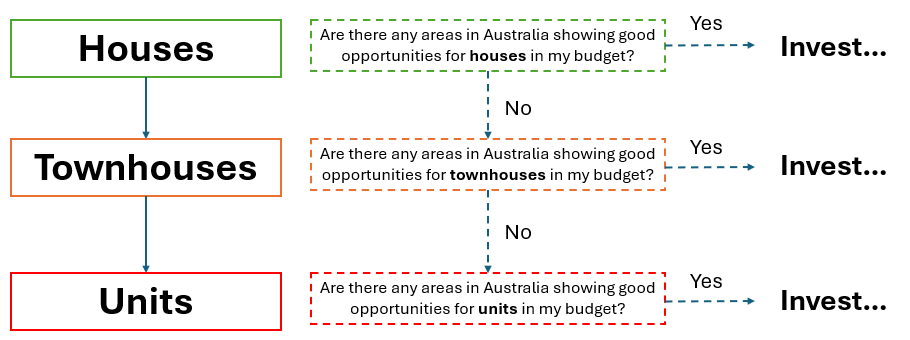

For the avoidance of doubt, let me share with you a very general asset hierarchy along with a thought process which may be useful for those first-time / newbie investors to reference.

So in essence, you want to be buying houses to the extent your budget permits and then move down the chain to townhouses then units. Please note that this is very general guidance and property investing is specific to each person so please take this with a grain salt. However, whilst there are going to be people that try to complicate things further and say the above is not nuanced enough blah blah blah - and to an extent they are correct, but the reality is that houses are the best performing asset in the real estate game.

So particularly for those of you who are at the start of your property investing journey - keep it simple for now and focus on acquiring houses (i.e. more land) provided the data and your budget supports this.

"But I live in [insert capital city] - I can't afford to buy a freestanding house!"

Well, that statement is only true if you are living in the 2000s and are only willing to purchase property in your own backyard. If you want to become a successful property investor in today's age, you need to embrace borderless investing, which is what we are discussing next.

Purchasing a house also comes with significantly less administrative issues and costs - in particular, there are no body corporate / strata fees which can be very expensive if you are silly enough to buy a unit in those brand new high-rise complexes with all the fancy amenities. You also have a lot more flexibility with what you want to do with your home; you can subdivide it or build a granny flat at the back (subject to council approval) or you can do a renovation on the inside of your home (which normally doesn't require council approval), whereas you typically can't do that in an apartment block without getting body corporate / strata approval.

For those of you who don't know what body corporate and strata is (two different but similar things) - give it a quick ChatGPT or check out this summary here. They are basically just a giant (and expensive) pain in the ass that are supposed to assist with the management and maintenance of the building / complex that a unit is located in.

Don't get me wrong - there are some downsides to investing in houses, with the main ones being that homes typically have lower rental yields and can have more maintenance costs; however, these are all outweighed by the difference in capital growth you receive from investing in houses compared to units.

Before the property gurus screenshot this section and film a cringey Instagram reel or TikTok on this - whether you should be investing in houses or units is not as black and white as this (but I am not too far off). Can units experience significant capital growth? Yep they definitely can, this often occurs after houses have become unaffordable in an area, so if you buy in the right time of the market cycle and invest in the correct type of unit you can make money. I will go through what a good unit investment is in the property selection criteria section of this website, but generally they are basic brick units with low body corporate fees and small complexes of 4 - 12 other units (i.e. you are buying a bigger chunk of the land and the land-to-asset ratio is better). But can a unit earn you more capital growth than a house? Yep it's more than possible, but as the data shows, this is an exception to the rule and would generally occur if you are investing in non-investment grade homes with lots of supply side risk and low demand - such as the house and land packages we discussed above.

I am not going to labor on too much more about this so if you want to hear more about this never-ending debate, check out the below YouTube videos.

So what about Townhouses (or Villas)?

All the arguments we have mentioned above essentially are applicable to townhouses for the same reasoning - they have a lower land component than houses and therefore they do not perform as well over the long term.

However, there is an argument to be made that townhouses can be seen as a somewhat 'middle ground' in order to allow investors to enter into those markets that are becoming increasingly unaffordable for the local demographic (e.g. capital cities such as Sydney, Brisbane, Melbourne… maybe even Adelaide now) whilst also obtaining a solid yield and land-to-asset ratio (ideally 50% or more).

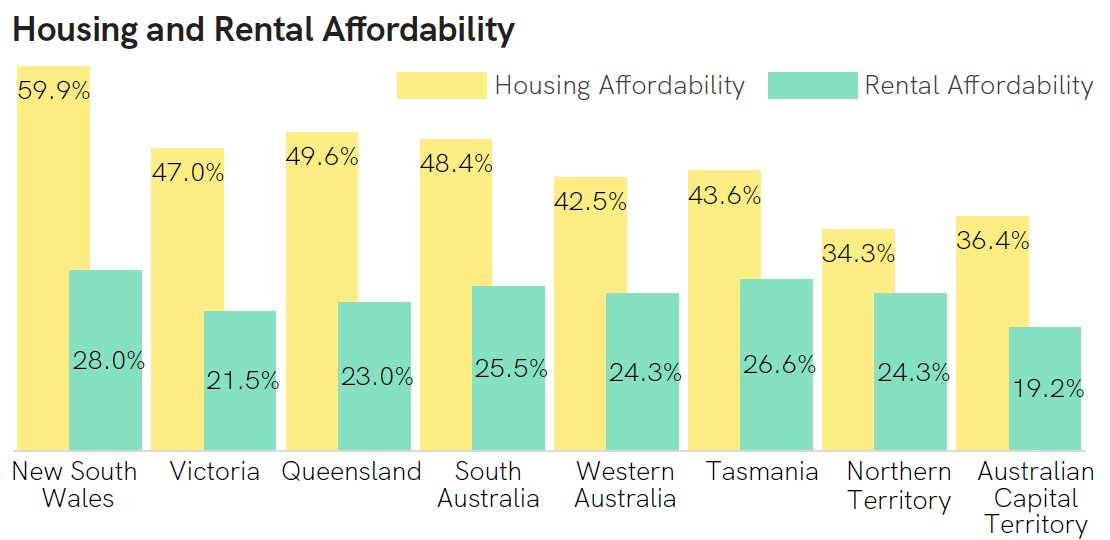

Or in other words, as housing affordability continues to worsen in Australia's major cities (see the below graph for reference - the higher the percentage the more unaffordable the area is) people will begin to gradually turn to the next most affordable option that offers them the most land - which is townhouses (and eventually units…).

This is especially true given the density of Australia in that over 50% of our population is crammed into three cities (being Sydney, Brisbane and Melbourne), so as our population increases so will the demand for land (resulting in an increase in land values) and therefore purchasing the right townhouse can be a viable option at the right price for those investors who want to get exposure to the more unaffordable capital cities in Australia.