Step 3 - Strategy Building

One of the more overwhelming topics to grasp as a newbie investor in my opinion is building your 'strategy'. I believe this is because most of the content online is produced by buyer's agents who want to intentionally make this more complicated than it needs to be so that you end up turning to their services for help.

So I am going to try and break it down as simple as possible so that you end up taking action.

Keep it Simple, Stupid - Buy and Hold

I know on this website I have criticized the way your parents may have invested in property quite a bit, but one thing they did do right is keep it simple. Most of the older generation didn't go around buying and selling out of markets like some sort of property day-trader, they focused on purchasing quality assets and holding them as long as they needed to.

That's all there really is to the 'buy and hold' strategy:

Use data to purchase a quality asset that will experience high capital growth over the short and long term;

Target a rental yield which is balanced enough so that you can hold the property for the foreseeable future; and

Rinse and repeat until you have enough of an asset base to achieve your financial goals.

Chances are if you have tried to research property strategies on the internet you will see that there are quite a few that the gurus are telling you to consider, including duplexes, rooming houses, building granny flats, development / subdivision, commercial properties, flipping and many more; however, all the best investors start their journey using the 'buy and hold' strategy.

This is because, when done properly, 'buy and hold' is the strategy with the least amount of risk (and upfront costs…) and places the most amount of focus on maximizing capital growth.

By focusing on capital growth early on in your property investing journey you are doing two key things: (1) taking advantage of compound interest / growth; and (2) giving yourself more flexibility and options in the future.

1. Taking advantage of compound interest / growth

What is compound interest / growth?

Albert Einstein described the phenomenon of compound interest as the "eighth wonder of the world", and once you see it in action it is pretty easy to see why.

For those who don't know, compound interest is the interest calculated on the initial principal amount that you invested plus the accumulated interest from previous periods, meaning you earn interest on the interest you have already earned.

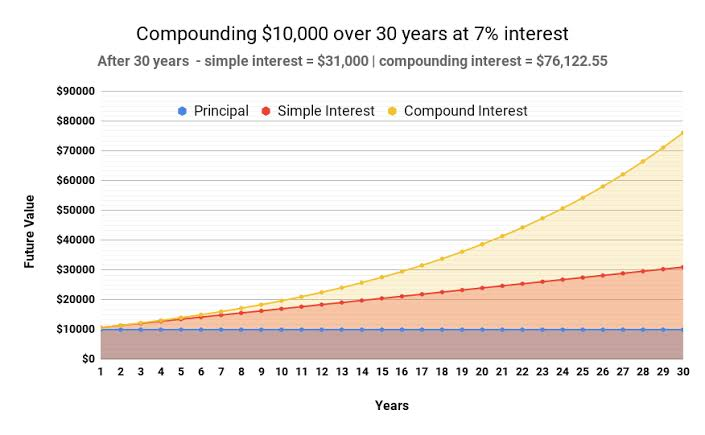

For example, imagine you put $10,000 in a savings account that pays 7% interest per year, and you do nothing and just let the interest compound - meaning each year’s interest is added to your balance, and then the next year you earn interest on that bigger balance.

After the first year, your $10,000 grows by 7% → that’s $700, so now you have $10,700.

In the second year, the bank doesn’t just pay interest on the original $10,000 - it pays the 7% interest on the full $10,700. So you earn $749 instead of $700, and your balance becomes $11,449.

You haven't invested / contributed any more money yourself into the account and you have earnt an extra $49 in one year compared to the previous year purely from compound interest. This will then continue to compound over the years and you will end up with a much larger sum that you originally invested (i.e. $76,122.55 after 30 years).

I always think this makes more sense visually so take a look at the this 30-year graph for reference.

Now the same principle applies to property investing, because the capital growth on your investment property will also compound on itself each year.

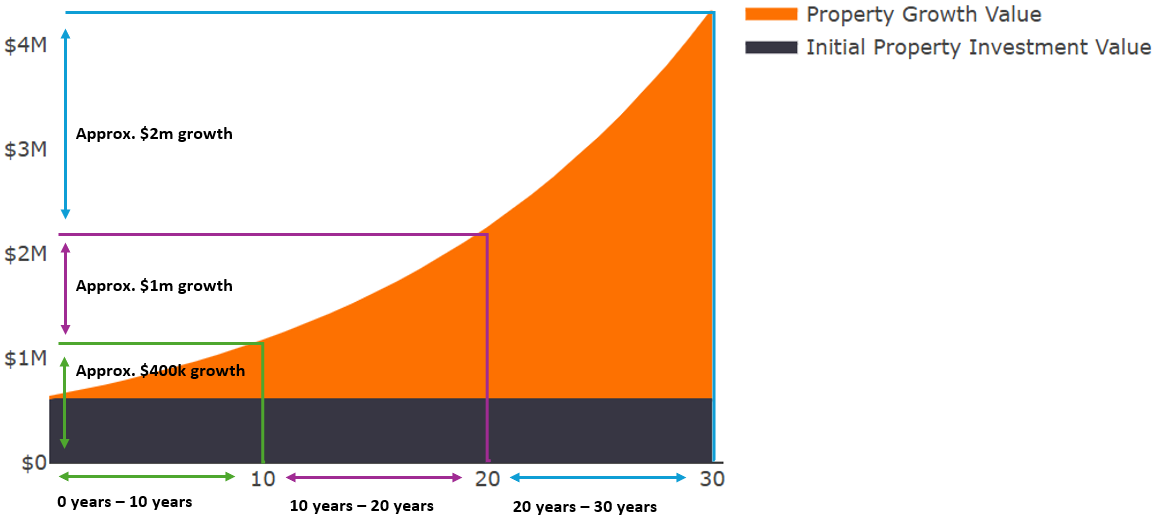

For example, let’s say you purchase a property for $600,000 and it rises at the at the national average of 6.8% per year - that 6.8% isn't just multiplied against the original purchase price you paid for the property, each year it is compounded against the new higher value from last year.

When you extrapolate this across a 30-year time period, this means a $600,000 property that performs at the national average (i.e. a standard investment property, you can do much better) would be valued at over $4,000,000… take a look at the below graph if you don't believe me.

Why does the 'buy and hold' strategy maximise the compounding effect?

If you have a keen-eye you may have noticed that on the graphs I have included above the amount of money you earn through compounding increases significantly after the first 10 years and even more after the first 20 years (and so on and so on…).

In case it is not clear, take a look at the jumps in value in the below graph, which is the same as the one above except I have segregated it into 10 year time periods. As you can see the graph clearly shows that if you want to make the most out of the compounding effect you need to be holding your property for a long term. Noting again, just to be 100% clear, your property won’t grow in a tidy upwards trajectory like the below graph indicates - this is just for illustrative purposes.

The beauty of property investing is that you didn't even invest all of the $600,000 from your pocket, instead you could have used anywhere from 5% - 20% of your own money for the deposit (plus stamp duty blah blah blah) then just use the bank's money for the rest - which means your cash-on-cash return is huge.

This is also just the results with one property at $600,000 - imagine you build a portfolio with a few of these at a similar or higher purchase price…

A few other things to note here:

As we know, in reality property doesn't actually grow at a flat consistent amount each year, it grows in cycles. That doesn't change the 30 year-end result you see above, it just means the graph isn't as neat and tidy as it is presented in these capital growth calculators (i.e. there should be ups and downs).

We have discussed this before, but the power of compound interest really reinforces why it is important to time your entry into a market so you maximise your short term growth, because you want the compounding to effect to be applied to the highest value you can achieve for the longest amount of time. If you time your entry right into a market you can makes hundreds of thousands (even millions) more in the long-run.

2. Giving yourself more flexibility and options in the future

Property investing is a journey and as you get more confident and experienced along this journey you may want to try out some of these different property strategies, such as pivoting into commercial property due its higher cash flow. By starting out using the 'buy and hold' strategy you are giving yourself the most flexibility as you are focusing on building out your asset base so that in the future, if you want to, you have the capital (i.e. money) to be able to sell-down or pull-out equity to allow you to pivot into other strategies which are more capital intensive (i.e. strategies that cost more money to get into than a simple buy and hold property investment).

What people also don't realize is that if you purchase a great buy and hold property it may also take you down many different strategies throughout the lifecycle of you holding that property. For example, if you a buy a property with a high land-to-asset ratio the chances are it is probably quite dated or in original condition - this gives you the opportunity to give it a cosmetic renovation down the track to increase its value. It probably also is on a bigger block size - potentially 600m2+, this means that depending on the planning rules in the area and the configuration of the land you could one day build a granny flat at the back of it to increase your cash flow or even subdivide it and build a completely new property that you could sell.

The point is, if you focus on keeping it simple and buying a quality asset to hold for a long period of time you give yourself options down the track as your personal situation or risk appetite changes over time - this is not always available to you if you start your journey off with more complicated / risky strategies.

Does that mean there are no situations in which you should sell your property?

Absolutely not, there are plenty of reasons why you may choose to sell a property before you retire, with the main one being your asset is underperforming (i.e. you have bought a dud) and / or it is preventing you from securing a better opportunity (i.e. the opportunity cost of holding the asset is greater than the value it is producing for you). Or maybe your personal circumstances have changed and you need / want the money now (e.g. to pay off the debt on your owner-occupier home) - it's all situational and your situation will change over the course of your investment journey.

But the point is, if you are new to investing you should keep it simple and buy a property with the intention of it giving you great short-term gains and being a good long-term hold, then you can always adapt your strategy if necessary as your journey progresses.

Now you may hear from some buyer's agents and property experts on the internet that it is more effective to continue to buy-in and sell-out of markets based on where they are in their market cycle. There is definitely some merit to this argument, but overall, in my opinion, the buying and selling costs are too high in Australia to make this a cost-effective strategy for the average investor (especially if you are paying a buyer’s agent $20k+ each time…).

If you want to see an analysis of the 'buy and hold' strategy against the 'buy and sell' strategy please check out the below video from Davey Hamilton who I think gives a great overview. Really suggest you watch this one so you can see that the profit that you think you are making when selling your investment property is normally much higher than what you actually receive when you consider all the transaction costs involved. For those interested in getting a greater understanding of the different types of property investing strategies here is also a video from Luke Wiles which grades them based on their risk level and focus on capital growth or cashflow.

Buyer Beware: Transactional Buyer's Agents

Before we move on, I wanted to note you should be very cautious of any buyer's agents promoting a 'buy and sell' strategy because it benefits them more than it benefits you, because the more times you buy a property with them the more fees you pay them. Some of them may say something along the lines of "our waitlist of clients is massive we don't need to tell our repeat clients to sell to collect more fees…" but what they don't tell you is that even if this is true it is more efficient for buyer's agents to work with repeat clients than new clients - deals get done quicker because trust has been built, that's why you will see buyer's agents always giving preference to repeat clients (nothing really wrong with this in my eyes as long as they are transparent about it, but it is something you should be aware of).

You should also be very cautious of the markets that these 'buy and sell' buyer's agents are putting you into as they may not be very economically diverse and therefore it could be a riskier investment than your risk appetite may tolerate. It could also be a market that is dominated by investors, so whilst you can make some money in the short-term there is a tangible risk that it could be very difficult to sell the property when it is time to exit if all other investors (or other clients of your buyer's agent) are thinking the same thing. Cough cough.. Darwin.. cough cough.

Remember that the success in a property investment is measured by its: (1) short term capital growth; and (2) long term capital growth. Buyer's agents will rarely be around to experience the consequences of their actions if they don't achieve consistent long-term growth given how long it will take to measure (i.e. 7 years +) and for this reason there can be some bad faith actors who will solely focus on locations that will only produce gains in the short-term but don't have the fundamentals for long-term growth. Cough cough.. DARWIN.. cough cough.