Step 1 - Understanding the Fundamentals

When you are investing in property the goal is not just to make some money or not lose money - you want to achieve the best return on investment possible. This is a key factor most people overlook…

This means you need to be putting your money into the best suburb for capital growth within your budget at the time you are investing. There are over 15,000 suburbs in Australia and the average person will only live in a few of these across their lifetime. So if you limit your investment choices to just those areas which you are familiar with (i.e. your backyard) then you are removing thousands of suburbs from your investment decision making process - leaving you with very limited options.

Think logically here - out of all suburbs in Australia, what are the chances that the one or two areas you are familiar with are the best areas in Australia for you to invest in at any given time. The probability is very very slim - that’s not just my opinion, it's a statistical reality.

Just think about some of the fundamentals you have learnt about on this website so far and you will clearly see how they don't align with the 'strategy' of just blindly investing in your own backyard:

Property Fundamental

The property market is very cyclical with some areas currently experiencing a 'boom' in prices, whilst some are about to start to see an 'upturn' in prices and others seeing a 'slump / stagnation' in prices.

Implications of the Backyard Approach

Land is what appreciates in value and for this reason houses are the best performing asset class in property investing.

Capital growth is the ultimate goal in property investing; however, you need to ensure you have a balanced yield so you can comfortably afford to hold your properties and continue to scale your portfolio.

Increases in house prices are caused through an imbalance between supply and demand which is assessed through various different data metrics.

Backyard Investor

By deciding that you are going to only invest in your backyard you are either doing one of following two things:

(a) not considering what point in the property cycle your backyard is in, meaning that you are running the risk that you are buying into the market at its peak or its downturn meaning you may see very limited growth for the foreseeable future; or

(b) you are aware of what point in the property cycle your backyard is in and have decided to invest in it anyway as you are focusing only on time in the market as opposed to timing your entry into the market, meaning that you are not making the best use of your money as it could be generating better returns in other markets and therefore you are incurring significant opportunity costs whilst paying the holding costs on asset that may not provide you noticeable capital growth for a long time.

Depending on where you live in Australia, you may not be able to afford a house in your backyard - this means you may need to compromise on the quality of the asset and purchase something with less land component (i.e. a townhouse or unit) just so that you can buy in that area. Therefore, you may achieve lower capital growth in the long-term then you would have if you purchased a house with land in another area.

The area you live in / are familiar with may be a more premium area with historically lower yields, meaning that holding the property may significantly impact your financial situation and prevent you from scaling your property portfolio any further as you won't be able to afford to hold any more properties.

Alternatively, you may live in an area that has very high yields but the economy is quite undiversified (i.e. a mining dominant town) and as a result the property prices in your backyard may be very volatile which significantly increases the risk that you may not achieve noticeable capital growth.

By blindly buying in your backyard you aren't considering the supply and demand dynamics - you are just winging it and hoping that prices will increase eventually.

The area you grew up in may have a lot of stock on market currently or maybe a developer has just been approved to build a bunch of new homes nearby, which may make it easier for you to buy but it won't do any wonders for house prices as there will be an influx of supply to the market. Additionally, houses may be sitting on the market for months on end in your backyard which indicates there is low demand in the area which also has a negative impact on house prices.

Can you make money investing in your own backyard? Yes of course, plenty of people have done it but for all these backyard success stories you need to consider the following questions:

Question 1: How long did they hold this property before they achieved meaningful capital growth?

Those who ignore market timing and just jump head first into buying a property in their own backyard can potentially wait many years before they experience any capital growth which they could extract as equity to fund their next purchase - in which time certain markets would have grown significantly more. As we have discussed throughout Step 1, this is why it is vital that you time your entry into the market appropriately so you can extract equity in the short / medium term.

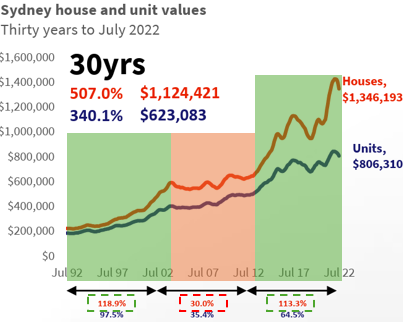

Just a take look at the below diagrams - if they look familiar it's because these are the charts from the Introduction where I also discussed this topic, but I thought it may be useful here to reiterate the point. For example, there will have been plenty of people living in Sydney who saw their friends / family buy a house in the late 90s and see it double within the space of 10 years - so what do they do? They got FOMO and jumped into the market because they knew no better and they thought "if Sydney doubled in last decade it will surely double again in the next decade!" Well they were wrong - instead Sydney only grew 30% from 2002 to 2012.

But the thing is you never hear this part of the story, you only ever hear about how much that Sydney house is worth after it eventually grew 113% from 2012 to 2022, completely ignoring the 10 years before that where they paid all the holding costs associated with owning the home all whilst it significantly underperformed the national average.

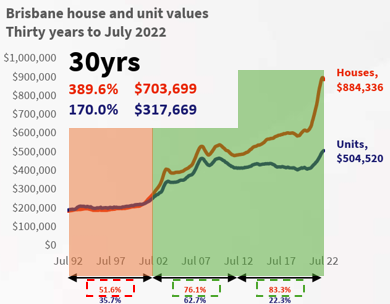

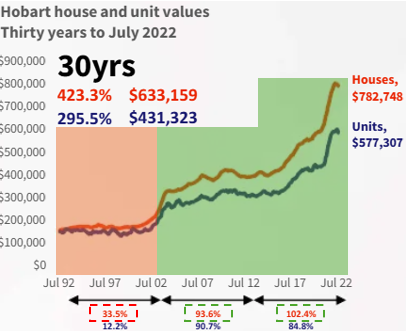

Meanwhile, what were the smart borderless investors doing? They were investing in areas like Brisbane which grew over 75%, or better yet Hobart which grew over 90% in the same decade that Sydney only grew by 30%. Then they may have entered in Sydney around 2012 so they could take advantage of eventual boom that the city experienced.

This means they minimized their opportunity cost and maximized the return on their cash by investing in the location that was about to enter the best time of the property cycle (i.e. remember the 'optimal buying window' which we discussed in the market cycle timing chapter of Step 1), not just the location that they grew up in...

Question 2: What data did they look at to give them the confidence to buy at that time?

On the other hand there are some backyard-only investors which manage to enter the market at a great time and they end up achieving significant capital growth in the short / medium term - you probably know some of them, or maybe you are one of them. However, I would be curious to know how they came to the decision that it was a good time to invest in the area they grew up in.

Most of them won't know about the metrics I will go through in Step 4 and they may have not even considered anything to do with supply and demand. Instead they probably did some form of basic qualitative analysis like "oh this is near a good school I know in the area and its close to public transport and shops…" - which is the extent to which most people perform property research in Australia.

The reality is that this type of investing is more akin to gambling - they got lucky. When I say 'lucky' I am using it more in a tongue-in-cheek way because ultimately they did take action which is the most important thing, you have to be in the game to have a chance at winning it. So honestly good on them and there are thousands of people just like them all over Australia, which is why there are so many people who feel qualified to put their two cents in on where you should buy property (me included lol).

However, the reality is that if you want to build a portfolio of properties (i.e. more than one or two) this type of success is just not replicable for the average person on a consistent basis or at scale - because as you now know, every market eventually goes through a 'slump' phase where prices decline or stagnate.

What will the backyard-only investors do during this phase? Just not invest? But that could means years on the sideline letting your money be eaten by inflation. Or do you just invest anyway and wait years before seeing any meaningful growth and pay all the holding costs whilst you wait? Both are bad options and are the inevitable consequences of restricting yourself to investing into only one area of a country.

Goverment Grants and Rentvesting

As I am sure you are well aware, the Government is basically just handing out money fresh off the print (literally…) to first home buyers to get votes to help them get on the property ladder. It should be said that if you purchase a property not in your backyard you won't be able to benefit from this free money.

The first thing you need to decide is are you buying a house to live in, or are you buying an investment. Or in other words, are you going to rentvest?

Rentvesting is the process whereby you rent where you want to live whilst simultaneously investing in properties elsewhere. I honestly would be very surprised if you haven't heard of this concept yet, but if not please go watch the below two videos and / or give it a Google as there is so much content on this (which gets very repetitive) that I don't think there is actually much value in me basically just re-explaining it. Ok see you again in 15 - 20mins!

I can't really help you too much on this decision, whether you want to rentvest or not is a personal choice and is going to be very dependent on your lifestyle and where you want to / currently live.

But in general, I would say that for most people living in major capital cities rentvesting (or living at home with your parents) is going to be the smartest option for building wealth - I do it, my partner does it and most other people I know with sizeable portfolios do the same.

The key point here is that you don't try and do both. When you go to buy a home to live in you are going to inevitably care more about the minor things which don’t have a major impact on the growth of the property, such as the kitchen bench materials, how new the bathroom is, what color the walls are etc. This type of emotional decision making is what makes people overpay or miss out on properties and it is this type of bias that you need to leave behind when buying an investment property.

"But stamp duty and LMI are so expensive, if I can avoid paying these costs why wouldn't I?"

I get it, purchasing your first property can be f***ing expensive if you don't take advantage of these grants, but you know what is more expensive? The opportunity cost of your first property being a dud investment.

Yes you saved $30,000 - 40,000, but as we have discussed above, what if the market you are buying in (i.e. your backyard) is at the peak or slump phase of its market cycle - you then run risk of your 'investment' (using that term very loosely here) going down in value or stagnating.

Whereas if you just said no to the grants from the Government and invested into a location interstate at the right time of the cycle you could instead make hundreds of thousands of dollars in capital growth - which would far outweigh the money you saved from not using the Government grants.

Depending on the value of the property you are buying interstate you may also not have to wait any longer to save the money for stamp duty because the property could be cheaper or the state you are buying in may charge less in stamp duty.

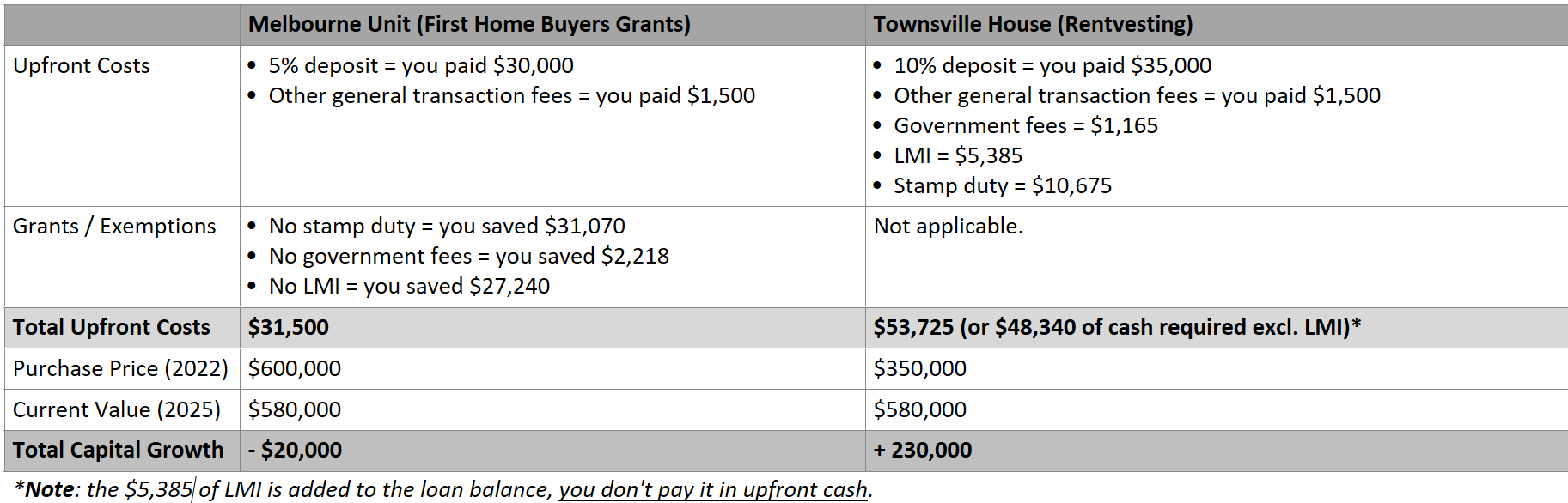

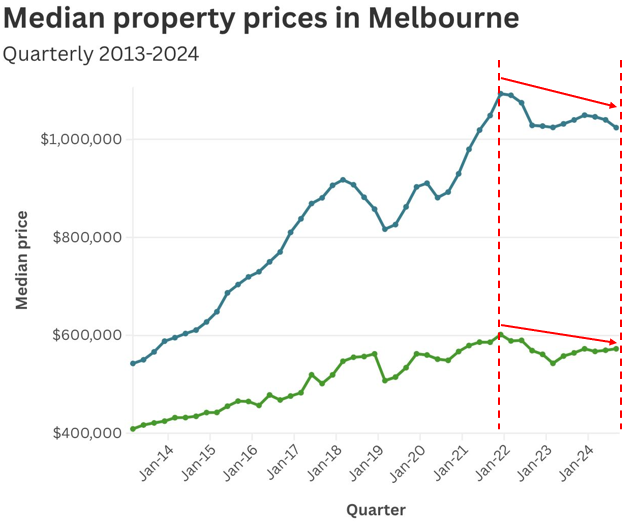

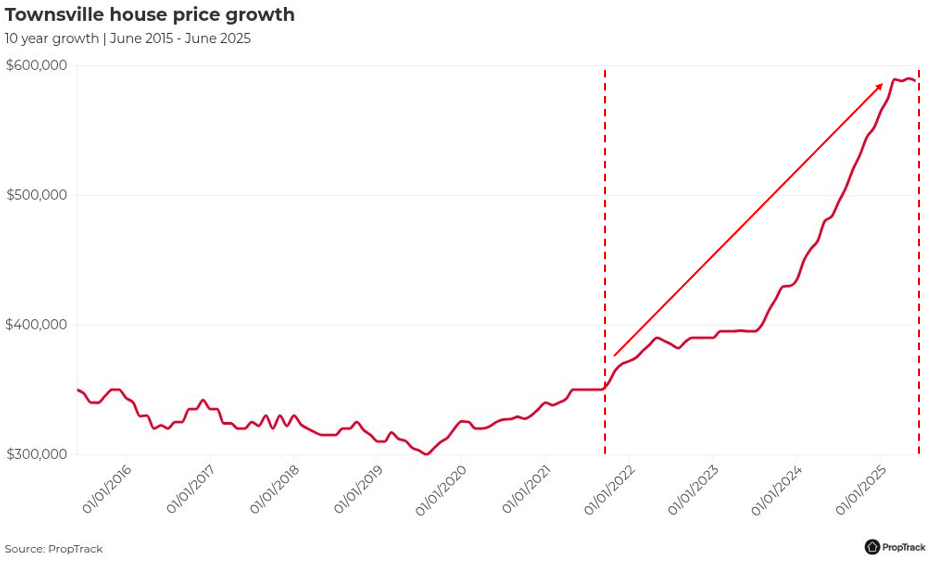

Let's take the Melbourne market as an example and let's assume you decided to purchase a unit in Melbourne for the median price of $600,000 back in 2022 - I am not too sure what grants were around that time, but to be conservative let's assume you got all the bells and whistles from the Government that we talk about today (before the mortgage brokers on reddit come at me, sorry if the maths is a little off - I am just trying to prove a general point here…):

How will I able to manage the property from interstate and make sure the tenant is not trashing the place, pays rent of time etc.?

How will I do my due diligence and inspect the property before buying it I don't see it before I buy it?

How will I know if the property is real and I am not getting scammed if I don't see it before I buy it?

As you can see, if you took advantage of the first home buyers grants and bought a unit in Melbourne you would have saved approx. $23,000 in upfront costs compared to the purchase in Townsville not using any government incentives; however, in three years' time your Melbourne unit would have actually decreased in value by $20,000, whereas the house in Townsville increased in value by $230,000. Ultimately, this means you would be have been better off by over $200,000 if you just ditched the first home buyers grant and instead invested in a location that was in the correct part of the property cycle and primed for growth.

I did exactly this and purchased in Townsville so I can vouch to the fact it is possible. Yes those deals in the $300,000 range are very difficult (if not impossible) to find in Australia these days but the specific examples and numbers here are not the point, all you need to do is understand the concept - the opportunity cost of taking advantage of first home buyer grants in a bad market will not outweigh the benefits from just investing in the best market at the time.

Please don’t obsess over the fact I used Townsville as an example here - this would’ve worked the same (if not better) if you bought in capital cities such as Perth, Adelaide or parts of Brisbane like Logan, Ipswich etc in 2022 instead.

Some of you may be wondering “What if the best market at the time is the area / state I am living in?”

Well if that’s actually true based on the data and you aren't just gaslighting yourself into believing that then congratulations you are very lucky, try take advantage of the best of both worlds - but for most people that won't be the case.

You got to see it to the believe it….apparently

The most common opposition I get from my friends and family when I tell them about borderless investing is that despite everything I have said above indicating that it makes complete sense from an investment perspective, they all say something along the lines of:

"But I want to be able to go and see the property so that's why I need to buy somewhere I can at least drive to…."

Why? Like seriously, why is that necessary?

You aren't going to drive past it every weekend to make sure it is still there are you? It’s a house, it's not going anywhere. Most of you probably have thousands of dollars sitting in your superannuation fund currently but I guarantee you aren't knocking on the door of your superfund asking to see how it's all going or request they only invest in shares of companies located within a driving distance of your house….. so why do it for an investment property?

I have put together a small table below of all the responses I usually get to that question along with my thoughts / response to help build your confidence with respect to borderless investing.

Borderless Investor

You will use a property manager. They will manage the property for you, shortlist the tenant candidates, collect rent, do inspections, liaise with trades regarding maintenance requests etc.

There are so many regulations these days between landlords and tenants you should never be self-managing your property in my opinion, even if you live next-door

Yes its costs money (not much in the grand scheme of things….), but it costs money to make money in property investing.

There are so many checks and balances in place to make sure you are not buying a property that doesn't exist.

You (or your buyers' agent) should be liaising with a real estate agent who will have an online presence which you can check, there may be a listing for the house and / or you can search it up on Google Maps street view, you will have a conveyancer who should be reviewing the title search of the property to ensure the owners match the sellers on the contract you sign, you should be performing a building and pest inspection in which case the building inspector will literally go to the property then send you a report on it and your bank will also perform their own checks, including doing a valuation on the home.

Just make sure you don't transfer anyone a house deposit before you have a signed contract that has been reviewed by your conveyancer who will then tell you when to transfer funds. Which is the exact same thing you should do when buying in your own backyard - so there is no difference.

First of all, as I will show you throughout this website, almost all due diligence on a property can be done remotely from your laptop (which I can almost guarantee you is what most buyer’s agent do these days), with the exception of inspecting the property.

Unless you are professional property inspector, veteran property manager, or maybe a builder - you should not be relying on your inspection of the property as the ‘be all and end all’ of whether you purchase a home, because the reality is you don't know what you are looking for. This applies whether or not you are purchasing in your own backyard or interstate. This is where you rely on your team of professionals.

For those of you who are using a buyers' agent, this is when you will need them to either attend or source detailed videos of the property and organize a building and pest inspection. Or for those who are doing it D.I.Y. you can ask property managers to inspect / view properties for you (a lot of buyer’s agents who operate nationally do this anyway) and you should be organizing a building and pest inspection.

We will get into the nitty gritty of the inspection process later on in this website, but the main point here is that each of these persons will know more than you about inspecting properties (maybe except the buyers' agent, given how atrocious some of them are these days) and so it is not necessary for you to actually be there and see the property - that is the reality.

If I am being honest, I have a lot of sympathy for that last reason - I totally understand how not seeing a home before you buy it can be nerve racking, especially given the size of the purchase.

However, what you need to get comfort from is that you are not just blindly purchasing this home - you are also getting feedback from professionals who know more than you. When you think of it like this, borderless investing can actually push you into undertaking more stringent and thorough due diligence as you are getting the help of experts as opposed to if you were purchasing in your backyard and decided to do all the inspections yourself.

For that reason, building your "team" is one the most important steps on your investment journey and coincidentally is what we are going to talk about next.